To secure these rights [of Life, Liberty, and the Pursuit of Happiness], Governments are instituted among Men, deriving their just powers from the consent of the governed...Whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government.

--Declaration of Independence

In the United States, secession as a valid strategy for coping with oppressive government goes at least as far back as Jefferson's words above. In the early 1800s, even outside observers such as Alexis de Tocqueville recognized the legitimacy of secession in the American system:

"The Union was formed by the voluntary agreement of the States; and in uniting together they have not forfeited their nationality, nor have they been reduced to the condition of one and the same people. If one of the states chooses to withdraw from the compact, it would be difficult to disprove its right of doing so, and the Federal Government would have no means of maintaining its claims directly either by force or right (1945: 381)."

Through the distortions of popular history, many think that the only movements toward secession in the United States were those by the Southern states prior to the Civil War. However, there were numerous threats of secession prior to 1860.

The Alien and Sedition Acts of the late 1790s drove resolutions drafted by Jefferson and Madison for Kentucky and Virginia that hinted at secession. In the early 1800s, several New England states believed that the economic policies enacted under the presidencies of Jefferson and Madison were disproportionately harmful to New England state interests (which mirrored arguments of Southern states under later administrations); the wisdom of secession was debated in Massachusetts, Connecticut, New York, and elsewhere over the span of at least 20 years.

As disagreements between Northern and Southern states got louder in the late 1850s, individual secession movements were spawned in several 'middle states' including New York, New Jersey, Pennsylvania, Delaware, and Maryland. Various themes drove these movements. Some states wanted to join the Southern Confederacy, some wanted to form a 'Central Confederacy,' and some simply preferred that the South should go in peace rather than destroying the Union by trying to hold it together by military force.

There was even some chatter in a few Northern states with abolitionist tendencies that Northern border states should secede in order to negate the federal Fugitive Slave Act, thereby making it easier for runaway slaves to escape.

By the time that Southern states undertook secession proceedings in 1860-1861, the right of states to secede was widely recognized and respected--even in the North. Historical studies of editorials from Northern newspapers (e.g., Perkins, 1964) clearly indicate that secession as a Constitutional right was broadly understood.

Lincoln sought to alter history by arguing that the federal Union preceded the states. He denounced the right of secession as 'an ingenious sophism.' Even in his Gettysburg address, at which time hundreds of thousands had already died from a conflict that he put in motion, Lincoln argued that representative government would 'perish from the earth' if the South won the war, and that the war was being fought in defense of government by consent.

The opposite was in fact true. If Southern states had been permitted to peacefully secede, two representative government would have existed--on in the North and one in the South. Moreover, it was clear that the Federal government under Lincoln sought to deny Southerners the right to government by consent, for Southern states, by their movement to secede, certainly did not consent to remaining in the Union.

The Civil War can be seen as Lincoln's war against the right of secession.

References

de Tocqueville, A. 1945. Democracy in America. New Rochelle, NY: Arlington House.

Perkins, H.C. 1964. Northern editorials on secession. Gloucester, MA: Peter Smith.

Friday, September 30, 2011

Thursday, September 29, 2011

A Better Idea

With a little perserverence you can get things done

Without the blind adherence that has conquered some

--Corey Hart

Leonard Read was a pioneer in questioning the sensibility of intellectual property protection. The basic argument is that 'ideas' cannot be claimed as property because the inputs employed have no clean title. That is, the ideas that I might 'create' are a composite of ideas/thoughts borrowed from others. It is impossible to separate the thoughts that are truly mine from thoughts that I may have borrowed from others.

Contrast this with property obtained by application of labor to raw materials and capital where ownership is clear. If I own the inputs, then the output is mine. If someone else owns the inputs, then the output is his/hers; as an employee, I essentially keep a portion of the output as my own based on whatever salary arrangement I have agreed to.

Read's point rings true. Ideas come from we know not where. They are not meant to be stored or monopolistically protected. They are meant to be shared--freely given as received.

Postscript: Leonard Read never copyrighted his work. He encouraged users of his work to copy it liberally. Very admirable.

Without the blind adherence that has conquered some

--Corey Hart

Leonard Read was a pioneer in questioning the sensibility of intellectual property protection. The basic argument is that 'ideas' cannot be claimed as property because the inputs employed have no clean title. That is, the ideas that I might 'create' are a composite of ideas/thoughts borrowed from others. It is impossible to separate the thoughts that are truly mine from thoughts that I may have borrowed from others.

Contrast this with property obtained by application of labor to raw materials and capital where ownership is clear. If I own the inputs, then the output is mine. If someone else owns the inputs, then the output is his/hers; as an employee, I essentially keep a portion of the output as my own based on whatever salary arrangement I have agreed to.

Read's point rings true. Ideas come from we know not where. They are not meant to be stored or monopolistically protected. They are meant to be shared--freely given as received.

Postscript: Leonard Read never copyrighted his work. He encouraged users of his work to copy it liberally. Very admirable.

Wednesday, September 28, 2011

Dr Copper

You had me down, twenty one to zip

Smile of Judas on your lip

Shake my fist, knock on wood

I've got it bad, and I've got it good

--Robert Palmer

Copper is often referred to as 'Dr Copper,' because it is said that the metal has a PhD in economic activity. The metal has so many uses that copper prices are thought to be a valid forecaster of economic strength.

What is Dr Copper telling us right now?

no positions

Smile of Judas on your lip

Shake my fist, knock on wood

I've got it bad, and I've got it good

--Robert Palmer

Copper is often referred to as 'Dr Copper,' because it is said that the metal has a PhD in economic activity. The metal has so many uses that copper prices are thought to be a valid forecaster of economic strength.

What is Dr Copper telling us right now?

no positions

Follow the Yellow Brick Road

"My, people come and go so quickly here!"

--Dorothy (The Wizard of Oz)

New knowledge for me here in the form of Rothbard's explanation of the dynamics surrounding the 1896 election. The election had become a referendum on the gold standard. During the early 1890s, the Democratic Party had largely been hijacked by a populist, infationist mindset led by presidential contender William Jennings Bryan.

Old School Democrats (the party of Jefferson), who were fiercely devoted to gold standard and sound currency, soured to this trend. The JP Morgan interest was part of the Old School Democrat gold standard crowd, although this group was interested in some government backing for a more 'elastic currency' to support the banks--particularly during times of crisis.

The Republican Party, dating back to its Whig and Lincolnian origins, was partial to inflation and central banking as well. By the late 1890s Rockefeller forces had become highly influential in shaping the Republican trajectory.

Seeing that the Democratic national convention of 1896 was likely to be won by the populists, Morgan reps approached Rockefeller reps to cut a deal. Morgan interests would support the Republican presidential candidate, William McKinley, provided that McKinley and the Republicans would pledge allegiance to a gold standard.

And so it went...

The gold standard pledge, of course, wasn't literal because plans were already in the works for a 'managed currency' and an institution to manage it. Such plans were antithical to the concept of a gold standard.

position in gold

--Dorothy (The Wizard of Oz)

New knowledge for me here in the form of Rothbard's explanation of the dynamics surrounding the 1896 election. The election had become a referendum on the gold standard. During the early 1890s, the Democratic Party had largely been hijacked by a populist, infationist mindset led by presidential contender William Jennings Bryan.

Old School Democrats (the party of Jefferson), who were fiercely devoted to gold standard and sound currency, soured to this trend. The JP Morgan interest was part of the Old School Democrat gold standard crowd, although this group was interested in some government backing for a more 'elastic currency' to support the banks--particularly during times of crisis.

The Republican Party, dating back to its Whig and Lincolnian origins, was partial to inflation and central banking as well. By the late 1890s Rockefeller forces had become highly influential in shaping the Republican trajectory.

Seeing that the Democratic national convention of 1896 was likely to be won by the populists, Morgan reps approached Rockefeller reps to cut a deal. Morgan interests would support the Republican presidential candidate, William McKinley, provided that McKinley and the Republicans would pledge allegiance to a gold standard.

And so it went...

The gold standard pledge, of course, wasn't literal because plans were already in the works for a 'managed currency' and an institution to manage it. Such plans were antithical to the concept of a gold standard.

position in gold

The Road thru Indy

"These people can make us disappear."

--Nina Chance (Murder at 1600)

Last week we noted Rothbard's knack for establishing the context of political decisions. Here is portion of his effort to piece together the network behind the organization of the Federal Reserve.

Center stage in this piece is the Indianapolis Monetary Convention of 1897, which subsequently become the Indianapolis Monetary Commission. The purpose of this commission was to begin a public relations effort to drum up support for 'banking reform'--a code name for central banking.

This group was laced w/ Morgan and Rockefeller representatives.

Note that although this special interest group succeeded in winning the ear of Congress by the end of the 1890s, it would still be a decade or more before the PR machine would win over enough support to enact the Federal Reserve. Why? Back then there was widespread distrust of central banking...two central banks had already been dismantled in the United States.

The propaganda machine still had work to do...

--Nina Chance (Murder at 1600)

Last week we noted Rothbard's knack for establishing the context of political decisions. Here is portion of his effort to piece together the network behind the organization of the Federal Reserve.

Center stage in this piece is the Indianapolis Monetary Convention of 1897, which subsequently become the Indianapolis Monetary Commission. The purpose of this commission was to begin a public relations effort to drum up support for 'banking reform'--a code name for central banking.

This group was laced w/ Morgan and Rockefeller representatives.

Note that although this special interest group succeeded in winning the ear of Congress by the end of the 1890s, it would still be a decade or more before the PR machine would win over enough support to enact the Federal Reserve. Why? Back then there was widespread distrust of central banking...two central banks had already been dismantled in the United States.

The propaganda machine still had work to do...

Tuesday, September 27, 2011

In Gold We Trust

I should have known better than to cheat a friend

And waste a chance that I'd been given

--Wham

As always, keen insight from Jim Grant. He argues that the price of gold = 1/T, where T is trust or confidence in the institution of managed (or fiat) currencies.

Is gold in a bubble. Wrong question says JG. The bubble driving gold price is government.com--absurd monetary and fiscal policy. Gold merely reflects merely reflects the absurdity.

Gold is a bet on the disorder produced by government.com

position in gold

And waste a chance that I'd been given

--Wham

As always, keen insight from Jim Grant. He argues that the price of gold = 1/T, where T is trust or confidence in the institution of managed (or fiat) currencies.

Is gold in a bubble. Wrong question says JG. The bubble driving gold price is government.com--absurd monetary and fiscal policy. Gold merely reflects merely reflects the absurdity.

Gold is a bet on the disorder produced by government.com

position in gold

Monday, September 26, 2011

Ponzi de Jour

If I'm losing control would you turn me away?

Or touch me deep inside?

And before this gets old

Will it still feel the same?

There's no way this could die

--Pat Benatar

The idea de jour in the EU crisis is to have governments borrow money from the ECB to buy assets (such as Greek bonds) from struggling banks. The vehicle for doing this is the EFSF (European Financial Stabilization Facility), which is a special purpose vehicle (SPV) established in 2010 and backed by EU country guarantees. The EFSF provides assistance to eurozone states in financial difficulty. The EFSF would essentially borrow using their country's assets as collateral.

The size of the borrowings necessary? Perhaps $1-2 trillion...

If this sounds like a version of TARP, then you'd be somewhat correct since the focus would be buying 'troubled assets.' In the case of TARP, however, government funds bought troubled assets from private sector banks. Under the latest EU plan, government money would be levered up with ECB money (more government money) to buy bonds from the same governments on the hook for the EFSF and ECB money to begin with.

How long before Mr Ponzi enters this discussion?

The only way such a program could be marginally effective is if Germany and France absorb an outsized share of the risk--well beyond what they have currently committed to contribute.

Which brings us back to the conclusion we've been reaching for months (here, here). Should Germany decide not to participate, then it all crumbles, cookie.

For today, anyway, markets were willing to look at the glass half full side of the story, with domestic markets up a couple of percent or so on the prospect of a $trillion EU bail out.

position in SPX

Or touch me deep inside?

And before this gets old

Will it still feel the same?

There's no way this could die

--Pat Benatar

The idea de jour in the EU crisis is to have governments borrow money from the ECB to buy assets (such as Greek bonds) from struggling banks. The vehicle for doing this is the EFSF (European Financial Stabilization Facility), which is a special purpose vehicle (SPV) established in 2010 and backed by EU country guarantees. The EFSF provides assistance to eurozone states in financial difficulty. The EFSF would essentially borrow using their country's assets as collateral.

The size of the borrowings necessary? Perhaps $1-2 trillion...

If this sounds like a version of TARP, then you'd be somewhat correct since the focus would be buying 'troubled assets.' In the case of TARP, however, government funds bought troubled assets from private sector banks. Under the latest EU plan, government money would be levered up with ECB money (more government money) to buy bonds from the same governments on the hook for the EFSF and ECB money to begin with.

How long before Mr Ponzi enters this discussion?

The only way such a program could be marginally effective is if Germany and France absorb an outsized share of the risk--well beyond what they have currently committed to contribute.

Which brings us back to the conclusion we've been reaching for months (here, here). Should Germany decide not to participate, then it all crumbles, cookie.

For today, anyway, markets were willing to look at the glass half full side of the story, with domestic markets up a couple of percent or so on the prospect of a $trillion EU bail out.

position in SPX

Sunday, September 25, 2011

Antecedents of the Civil War Part III

"I presume you all know who I am. I am humble Abraham Lincoln. I have been solicited by many friends to become a candidate for the legislature. My politics are short and sweet, like the old woman's dance. I am in favor of a national bank...in favor of the internal improvements system and a high protective tariff."

--Abraham Lincoln 1832

Previously we observed the influence of the American System, particularly its protectionist plank, in weakening the South's allegience toward the union of states. The American System was a product of Henry Clay and the Whig party in the 1810s.

From the time he entered politics, Abraham Lincoln was a disciple of Henry Clay and the Whig agenda. In his near 30 yr political career leading up to the 1860 presidential election, Lincoln was frequently on the record as supporting all three planks of the American System: a national bank, government sponsored 'internal improvements,' and protectionist tariffs. Lincoln subsequently nailed those planks into his own presidential campaign platform in 1860.

By this time, many Southerners believed that the federal government had been acting unconstitutionally for years, particularly w.r.t. fiscal and trade policies. In the South's view, these policies were imposing disportionate harm on the South.

With Lincoln gaining support among influential Northern voting blocs, the South saw an individual who threatened to consolidate federal power into the creation of a centralized state or empire. The effect of this consolidation was feared to be massive economic plunder at the South's expense.

Many Southern states thus commenced secessesion proceedings during the 1860 presidential campaign year. The Morrill Tariff bill of 1860, which proposed raising tariffs 100% or more on some items, added fuel to the secession fire.

By spring 1861, newspapers in the North and South had been noting that economic issues were the primary driver behind the secession movement. In March 1861, for example, the Boston Transcript wrote:

"It does not require extraordinary sagacity to perceive that trade is perhaps the controlling motive operating to prevent the return of the seceding States to the Union...The mask has been thrown off, and it is apparent that the people of the principal seceding states are now for commercial independence."

The Confederate Constitution largely mirrored the US Constitution with the exception that is removed language that did not support free trade. Thus, the Confederate Constitution outlawed protectionist tariffs altogether in support of a free market environment.

Newspapers began connecting the dots, warning that if free trade were permitted to exist in the Southern states, then merchants in New Orleans, Charleston, and Savannah would take most trade from Northern ports. Consequently, wrote the Boston Transcript, "the entire Northwest must find it to their advantage to purchase their imported goods at New Orleans rather than at New York."

Herein lies the primary driver of the Civil War. The federal government had been intervening in markets for years, with the cost of these interventions being disproportionately borne by the South. Lincoln threatened to take this intervention to new heights. Southern states thus opted to secede, and build an economic system around free markets. Influential Northerners soon realized that free markets in the South would hammer the protected markets of the North.

Fear of economic loss motivated those influential Northerners, people with the means to do so, to see to it that a man was elected president who would use lethal force if necessary to keep the South from realizing economic freedom--an economic freedom that, if left unchecked, would destroy the North's profit center.

The Civil War, like most if not all wars that the US has subsequently engaged in, was a war enacted by the federal government to protect the interests of those who preferred to acquire wealth by political rather than economic means.

--Abraham Lincoln 1832

Previously we observed the influence of the American System, particularly its protectionist plank, in weakening the South's allegience toward the union of states. The American System was a product of Henry Clay and the Whig party in the 1810s.

From the time he entered politics, Abraham Lincoln was a disciple of Henry Clay and the Whig agenda. In his near 30 yr political career leading up to the 1860 presidential election, Lincoln was frequently on the record as supporting all three planks of the American System: a national bank, government sponsored 'internal improvements,' and protectionist tariffs. Lincoln subsequently nailed those planks into his own presidential campaign platform in 1860.

By this time, many Southerners believed that the federal government had been acting unconstitutionally for years, particularly w.r.t. fiscal and trade policies. In the South's view, these policies were imposing disportionate harm on the South.

With Lincoln gaining support among influential Northern voting blocs, the South saw an individual who threatened to consolidate federal power into the creation of a centralized state or empire. The effect of this consolidation was feared to be massive economic plunder at the South's expense.

Many Southern states thus commenced secessesion proceedings during the 1860 presidential campaign year. The Morrill Tariff bill of 1860, which proposed raising tariffs 100% or more on some items, added fuel to the secession fire.

By spring 1861, newspapers in the North and South had been noting that economic issues were the primary driver behind the secession movement. In March 1861, for example, the Boston Transcript wrote:

"It does not require extraordinary sagacity to perceive that trade is perhaps the controlling motive operating to prevent the return of the seceding States to the Union...The mask has been thrown off, and it is apparent that the people of the principal seceding states are now for commercial independence."

The Confederate Constitution largely mirrored the US Constitution with the exception that is removed language that did not support free trade. Thus, the Confederate Constitution outlawed protectionist tariffs altogether in support of a free market environment.

Newspapers began connecting the dots, warning that if free trade were permitted to exist in the Southern states, then merchants in New Orleans, Charleston, and Savannah would take most trade from Northern ports. Consequently, wrote the Boston Transcript, "the entire Northwest must find it to their advantage to purchase their imported goods at New Orleans rather than at New York."

Herein lies the primary driver of the Civil War. The federal government had been intervening in markets for years, with the cost of these interventions being disproportionately borne by the South. Lincoln threatened to take this intervention to new heights. Southern states thus opted to secede, and build an economic system around free markets. Influential Northerners soon realized that free markets in the South would hammer the protected markets of the North.

Fear of economic loss motivated those influential Northerners, people with the means to do so, to see to it that a man was elected president who would use lethal force if necessary to keep the South from realizing economic freedom--an economic freedom that, if left unchecked, would destroy the North's profit center.

The Civil War, like most if not all wars that the US has subsequently engaged in, was a war enacted by the federal government to protect the interests of those who preferred to acquire wealth by political rather than economic means.

Yield Detention

Love's strange so real in the dark

Think of the tender things that we were working on

Slow change may pull us apart

When the light gets into your heart, baby

--Simple Minds

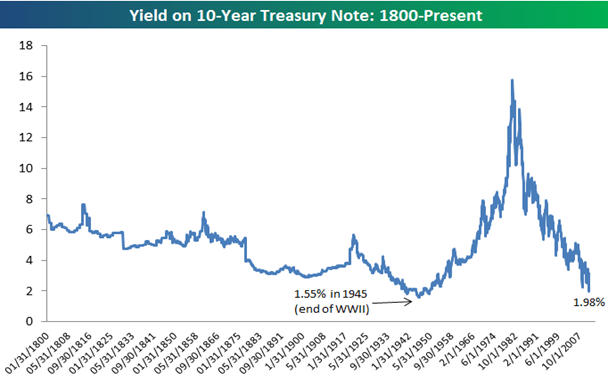

Below is monthly chart of the yield on a ten year Treasury note over the past 20 years. Earlier this month 10 yr yields dropped below 2% for the first time ever.

After the Fed announced Operation Twist this past wk, yields broke lower yet again. They now reside at about 1.8%.

The Fed is trying to buoy economic activity thru borrowing--particularly w.r.t. housing. But anyone with a pulse recognizes that interest rates, which have been at generational lows for months, do not constitute a binding constraint on economic activity here. Economies around the world are already choking on debt and have little appetite for more. The Fed is thus pushing on a string.

Two groups are especially hurt by Fed policy here. Retired people and other savers are having trouble making ends meet as it is becoming impossible to make ends meet by making 1-2% off modest principal. Savings are being gutted by Fed policy. Moreover, low returns on savings are nudging more people into risky assets such as dividend-paying stocks.

Keep in mind that, over time, savings are the driver of higher standard of living as resources set aside are invested in productivity-enhancing technologies.

Pension funds are also significantly impacted by long bond rates. Pensions funds are built on bond portfolios, and these portfolios are returning less and less. Lower bond yields increase pension fund assumptions about future liabilities, thereby creating funding gaps. To close these gaps, pension fund managers can take more risk increasing their allocation towards stocks, or, in the case of corporate pension funds, have the corporate parents write checks out of retained earnings to fund the shortfall. Those checks in turn reduce earnings...

By discouraging saving and encouraging risk taking, current Fed policy serves as a major drag on standard of living.

position in SPX

Think of the tender things that we were working on

Slow change may pull us apart

When the light gets into your heart, baby

--Simple Minds

Below is monthly chart of the yield on a ten year Treasury note over the past 20 years. Earlier this month 10 yr yields dropped below 2% for the first time ever.

After the Fed announced Operation Twist this past wk, yields broke lower yet again. They now reside at about 1.8%.

The Fed is trying to buoy economic activity thru borrowing--particularly w.r.t. housing. But anyone with a pulse recognizes that interest rates, which have been at generational lows for months, do not constitute a binding constraint on economic activity here. Economies around the world are already choking on debt and have little appetite for more. The Fed is thus pushing on a string.

Two groups are especially hurt by Fed policy here. Retired people and other savers are having trouble making ends meet as it is becoming impossible to make ends meet by making 1-2% off modest principal. Savings are being gutted by Fed policy. Moreover, low returns on savings are nudging more people into risky assets such as dividend-paying stocks.

Keep in mind that, over time, savings are the driver of higher standard of living as resources set aside are invested in productivity-enhancing technologies.

Pension funds are also significantly impacted by long bond rates. Pensions funds are built on bond portfolios, and these portfolios are returning less and less. Lower bond yields increase pension fund assumptions about future liabilities, thereby creating funding gaps. To close these gaps, pension fund managers can take more risk increasing their allocation towards stocks, or, in the case of corporate pension funds, have the corporate parents write checks out of retained earnings to fund the shortfall. Those checks in turn reduce earnings...

By discouraging saving and encouraging risk taking, current Fed policy serves as a major drag on standard of living.

position in SPX

Saturday, September 24, 2011

The Social Contract Fallacy

Welcome to your life

There's no turning back

Even while you sleep

We will find you

--Tears for Fears

Hoping to increase support for legitimizing plunder of property from wealthy citizens, the Left is rolling out the tired social contract argument. This time around, it appears to have been tendered by a woman from Massachessetts running for Senate.

In the tax-the-rich context, the social contract argument posits that wealthy people get rich by using infrastructure (i.e., workers educated in public schools, goods moved on public roads, etc) that has been paid for by 'society.' Because that wealth was acquired on the back of 'society', then rich people are getting a 'free ride' on society's back unless they surrender a significant portion of that wealth under penalty of force in the name of giving back.

This argument is laughable right out of the gate. The notion that the wealthy are getting a free ride by using public infrastructure is absurd, since the lopsided nature of the current tax code means that rich people have funded the lion's share of public infrastructure. Indeed, a more valid argument is that it is the near 50% of adults that pay no income taxes who are getting a free ride on the backs of the rich.

Another problem with the social contract argument is that society is not a contractual entity. Society is a construct that exists only in people minds. It may serve a legitimate purpose in some situations to support generalization across many individuals. But society is merely an aggregate of individuals, all with different wants and needs. Exchange occurs between individuals. An argument that places a monolithic society on one side of the table and an individual on the other in a contractual context is a fiction contrived to influence weak minds.

Perhaps the most glaring problem with the social contract argument is that there can be no implied contract between any individual and some aggregate entity. A contract is an agreement of exchange made voluntarily between two parties. Proponents of the social contract argue that simply being born into a community activates a contract that legitimizes expropriation of property to some other entity. But this argument merely imposes conditions of despotism and serfdom rather than voluntary contracting. That an individual lives in a community and pays taxes does not imply consent of contract to do so.

Can it be said that slaves who do not attempt escape consent to a contract of servitude?

Moreover, in the tax-the-rich context, it is apparent that supporters of the social contract agreement believe that the terms of the contract, e.g., the rate at which wealthy must surrender their property, can be arbitrarily renegotiated by the 'society' side of the table. Contracts do not permit arbitrary, one-sided revision.

The social contract argument is a rationalization for depotism and serfdom.

There's no turning back

Even while you sleep

We will find you

--Tears for Fears

Hoping to increase support for legitimizing plunder of property from wealthy citizens, the Left is rolling out the tired social contract argument. This time around, it appears to have been tendered by a woman from Massachessetts running for Senate.

In the tax-the-rich context, the social contract argument posits that wealthy people get rich by using infrastructure (i.e., workers educated in public schools, goods moved on public roads, etc) that has been paid for by 'society.' Because that wealth was acquired on the back of 'society', then rich people are getting a 'free ride' on society's back unless they surrender a significant portion of that wealth under penalty of force in the name of giving back.

This argument is laughable right out of the gate. The notion that the wealthy are getting a free ride by using public infrastructure is absurd, since the lopsided nature of the current tax code means that rich people have funded the lion's share of public infrastructure. Indeed, a more valid argument is that it is the near 50% of adults that pay no income taxes who are getting a free ride on the backs of the rich.

Another problem with the social contract argument is that society is not a contractual entity. Society is a construct that exists only in people minds. It may serve a legitimate purpose in some situations to support generalization across many individuals. But society is merely an aggregate of individuals, all with different wants and needs. Exchange occurs between individuals. An argument that places a monolithic society on one side of the table and an individual on the other in a contractual context is a fiction contrived to influence weak minds.

Perhaps the most glaring problem with the social contract argument is that there can be no implied contract between any individual and some aggregate entity. A contract is an agreement of exchange made voluntarily between two parties. Proponents of the social contract argue that simply being born into a community activates a contract that legitimizes expropriation of property to some other entity. But this argument merely imposes conditions of despotism and serfdom rather than voluntary contracting. That an individual lives in a community and pays taxes does not imply consent of contract to do so.

Can it be said that slaves who do not attempt escape consent to a contract of servitude?

Moreover, in the tax-the-rich context, it is apparent that supporters of the social contract agreement believe that the terms of the contract, e.g., the rate at which wealthy must surrender their property, can be arbitrarily renegotiated by the 'society' side of the table. Contracts do not permit arbitrary, one-sided revision.

The social contract argument is a rationalization for depotism and serfdom.

Friday, September 23, 2011

Conditions for Big Debt

"Watch that purgatory they call a gym. No shots six foot in. That'll do."

--Wilbur "Shooter" Flatch (Hoosiers)

Despite its pretty common title, I found this little article remarkably salient. The author argues that the only way that if debt was created in proportion to economic growth, which is how it would grow in an unhampered market over time, then there is no way our debt levels would be so out of whack.

Debt can only be created in the quantities that we currently deal with when financial institutions can lend new money, unbacked by real income, into existence. The root cause of the problem, he suggests, is fractional reserve banking.

Of course, fractional reserve banking can occur in an unhampered economy. Indeed, the 1800s saw many banks lending out more than they took in. In free markets, however, leveraged banks are prone to getting wiped out when risk appetites turn. Over time, depositers are likely to think twice about putting money into leveraged institutions because of the fear of banks runs.

In a free market, then, the amount of leverage banks can take on is likely to be modest at best.

Enter the central bank--in the US case this is the Federal Reserve. Central banks provide a backstop for leveraged banks in times of crisis. They can inject capital into member banks to prop them up and keep them solvent.

However, central bank support can only go so far when a currency is backed by gold, since money cannot be created in sufficient quantities to cover high levels of leverage.

Thus, the gold standard needed to be eliminated. This was done over a period of years once the Fed commenced operations after its 1913 charter. A major was the confiscation of gold from the citizenry in the early 1930s. Unpegging the dollar from gold literally gave the Fed a license to printing unlimited quantities of dollars to liquify overleveraged banks during crises.

Even under these conditions, however, a shadow of doubt might rest in depositor's minds about the soundness of banks in any condition. To alleviate those fears, government-sponsored deposit insurance (FDIC et al) was provided so that bank customers no longer thought twice about the safety of their deposits. Moral hazard becomes de rigueur...

And there you have it. A basic four point program for creating massive quantities of debt over time.

1) fractional reserve banking

2) central banks

3) remove link between currency and gold

4) government sponsored deposit insurance

--Wilbur "Shooter" Flatch (Hoosiers)

Despite its pretty common title, I found this little article remarkably salient. The author argues that the only way that if debt was created in proportion to economic growth, which is how it would grow in an unhampered market over time, then there is no way our debt levels would be so out of whack.

Debt can only be created in the quantities that we currently deal with when financial institutions can lend new money, unbacked by real income, into existence. The root cause of the problem, he suggests, is fractional reserve banking.

Of course, fractional reserve banking can occur in an unhampered economy. Indeed, the 1800s saw many banks lending out more than they took in. In free markets, however, leveraged banks are prone to getting wiped out when risk appetites turn. Over time, depositers are likely to think twice about putting money into leveraged institutions because of the fear of banks runs.

In a free market, then, the amount of leverage banks can take on is likely to be modest at best.

Enter the central bank--in the US case this is the Federal Reserve. Central banks provide a backstop for leveraged banks in times of crisis. They can inject capital into member banks to prop them up and keep them solvent.

However, central bank support can only go so far when a currency is backed by gold, since money cannot be created in sufficient quantities to cover high levels of leverage.

Thus, the gold standard needed to be eliminated. This was done over a period of years once the Fed commenced operations after its 1913 charter. A major was the confiscation of gold from the citizenry in the early 1930s. Unpegging the dollar from gold literally gave the Fed a license to printing unlimited quantities of dollars to liquify overleveraged banks during crises.

Even under these conditions, however, a shadow of doubt might rest in depositor's minds about the soundness of banks in any condition. To alleviate those fears, government-sponsored deposit insurance (FDIC et al) was provided so that bank customers no longer thought twice about the safety of their deposits. Moral hazard becomes de rigueur...

And there you have it. A basic four point program for creating massive quantities of debt over time.

1) fractional reserve banking

2) central banks

3) remove link between currency and gold

4) government sponsored deposit insurance

Smelt Fry

Dream of better lives the kind that never hate

Wrapped in a state of imaginary grace

I made a pilgrimage to save this human's race

Never comprehending the race had long gone by

--Modern English

Precious metals getting smelted today with gold down almost $90 and silver off by nearly 15% (!). Obviously my small venture into SLV yesterday wasn't the best of timing...

Support for GLD looks to correspond to the multi-year uptrend line which corresponds to 152ish.

SLV looks to have support right around here at 30, although it doesn't feel very strong. Stronger support may reside below at 25-26ish.

Have taken 'placeholder' positions in both metals and will be a better buyer lower.

positions in GLD, SLV

Wrapped in a state of imaginary grace

I made a pilgrimage to save this human's race

Never comprehending the race had long gone by

--Modern English

Precious metals getting smelted today with gold down almost $90 and silver off by nearly 15% (!). Obviously my small venture into SLV yesterday wasn't the best of timing...

Support for GLD looks to correspond to the multi-year uptrend line which corresponds to 152ish.

SLV looks to have support right around here at 30, although it doesn't feel very strong. Stronger support may reside below at 25-26ish.

Have taken 'placeholder' positions in both metals and will be a better buyer lower.

positions in GLD, SLV

Thursday, September 22, 2011

Battlefield 1120

You're making me go

You're begging me to stay

Why do you hurt me so bad?

--Pat Benatar

Domestic equities gapped about 3% lower after dismal overseas response to yesterday's FOMC announcement (plus continued deterioration in Europe).

They 'felt' lower in early morning trading as well. Early afternoon saw the SPX toying w/ the Aug closing low of 1120. This was the battleground for the remainder of the day.

I covered 20% of my short position during the probes of 1120. I intended to cover more if sell stops were tagged and sucked the index lower but that didn't happen.

I also bought a little SLV as silver was tagged for nearly 10%.

Stochastics suggest that the SPX is not all that oversold--unlike previous visits to 1120. Thus, there may be more downside 'energy' for piercing support. Classic technical analysis says the more times support is tested the weaker it gets. And today's back and forth around 1120 likely chewed through a few layers of latent demand.

Futes are up a few after hours, but would think that we see a probe lower in the near future.

position in SPX, SLV

You're begging me to stay

Why do you hurt me so bad?

--Pat Benatar

Domestic equities gapped about 3% lower after dismal overseas response to yesterday's FOMC announcement (plus continued deterioration in Europe).

They 'felt' lower in early morning trading as well. Early afternoon saw the SPX toying w/ the Aug closing low of 1120. This was the battleground for the remainder of the day.

I covered 20% of my short position during the probes of 1120. I intended to cover more if sell stops were tagged and sucked the index lower but that didn't happen.

I also bought a little SLV as silver was tagged for nearly 10%.

Stochastics suggest that the SPX is not all that oversold--unlike previous visits to 1120. Thus, there may be more downside 'energy' for piercing support. Classic technical analysis says the more times support is tested the weaker it gets. And today's back and forth around 1120 likely chewed through a few layers of latent demand.

Futes are up a few after hours, but would think that we see a probe lower in the near future.

position in SPX, SLV

Twist and Shout

You know you got me going now

Got me going

Just like I knew you would

Like I knew you would

--The Beatles

The new policy addition articulated in the FOMC statement yesterday is what has become known as Operation Twist. The idea is to 'twist' the yield curve by selling short term treasuries and buying long term ones.

The thesis being offered by the Fed is that Twist will further reduce long term interest rates and perhaps spur borrowing.

With rates already at generational lows, it should be clear to anyone with eyes that interest rates do not constitute a binding constraint on economic activity at present. There is little willingness to take on risk here by both lenders and borrowers. Stated differently, the world is already drowning in debt and doesn't want any more--even at cheaper prices.

What really perplexes me about Twist is that it doesn't just 'twist' the yield curve...it flattens it. A flatter yield curve is unfriendly to any institution engaged in the carry trade. Thus, banks, hedge funds, and other speculative entities seem likely to reduce investment risk in the face of Operations Twist.

Because the Fed 'needs' the participation of leveraged speculators to prop up risky asset prices, how the Fed sees value in Operation Twist is hard for me to figure.

position in SPX

Got me going

Just like I knew you would

Like I knew you would

--The Beatles

The new policy addition articulated in the FOMC statement yesterday is what has become known as Operation Twist. The idea is to 'twist' the yield curve by selling short term treasuries and buying long term ones.

The thesis being offered by the Fed is that Twist will further reduce long term interest rates and perhaps spur borrowing.

With rates already at generational lows, it should be clear to anyone with eyes that interest rates do not constitute a binding constraint on economic activity at present. There is little willingness to take on risk here by both lenders and borrowers. Stated differently, the world is already drowning in debt and doesn't want any more--even at cheaper prices.

What really perplexes me about Twist is that it doesn't just 'twist' the yield curve...it flattens it. A flatter yield curve is unfriendly to any institution engaged in the carry trade. Thus, banks, hedge funds, and other speculative entities seem likely to reduce investment risk in the face of Operations Twist.

Because the Fed 'needs' the participation of leveraged speculators to prop up risky asset prices, how the Fed sees value in Operation Twist is hard for me to figure.

position in SPX

Wednesday, September 21, 2011

Drain Opener

Here comes the rain again

Raining in my head like a tragedy

Tearing me apart like a new emotion

--Eurythmics

Looks like the FOMC statement did not contain enough goodies for the addicts, and markets subsequently drained. SPX was down about 3%, with things really letting go in the last half hour.

While we're still some distance from the August lows in the SPX, other 'tells' hint that a date with those lows may be coming.

The Trannies, for example, were splattered for more than 5% today and are now within spitting distances of their recent lows.

Will be interesting to see how overnight markets, particularly Europe, greet the FOMC decision.

position in SPX

Raining in my head like a tragedy

Tearing me apart like a new emotion

--Eurythmics

Looks like the FOMC statement did not contain enough goodies for the addicts, and markets subsequently drained. SPX was down about 3%, with things really letting go in the last half hour.

While we're still some distance from the August lows in the SPX, other 'tells' hint that a date with those lows may be coming.

The Trannies, for example, were splattered for more than 5% today and are now within spitting distances of their recent lows.

Will be interesting to see how overnight markets, particularly Europe, greet the FOMC decision.

position in SPX

Regulatory Irony

An old man turned ninety-eight

He won the lottery and died the next day

It's a black fly in your chardonnay

It's a death row pardon two minutes late

--Alanis Morisette

Nice rant by Peter Schiff on the stifling nature of government regulation. He makes a major point just past the three minute mark. The primary impact of industry regs is to shield major firms from competition. That competition comes from smaller firms and potential entrants.

Regs levy an outsized burden on small firms and often suffocate them. Regs discourage entry from entrepreneurs.

Unfortunately, a stack of research suggests that small firms and new entrants supply the lion's share of innovation to an industry (e.g., Christensen, 1997).

This is the irony of regulations. It is often said that regulations are necessary to 'protect' the consumer. But it is easy to argue that the primary protection consumers get from regs is protection from a major source of innovation that could improve standard of living.

Reference

Christensen, C.M. 1997. The innovator's dilemma. Cambridge, MA: Harvard Business School Press.

He won the lottery and died the next day

It's a black fly in your chardonnay

It's a death row pardon two minutes late

--Alanis Morisette

Nice rant by Peter Schiff on the stifling nature of government regulation. He makes a major point just past the three minute mark. The primary impact of industry regs is to shield major firms from competition. That competition comes from smaller firms and potential entrants.

Regs levy an outsized burden on small firms and often suffocate them. Regs discourage entry from entrepreneurs.

Unfortunately, a stack of research suggests that small firms and new entrants supply the lion's share of innovation to an industry (e.g., Christensen, 1997).

This is the irony of regulations. It is often said that regulations are necessary to 'protect' the consumer. But it is easy to argue that the primary protection consumers get from regs is protection from a major source of innovation that could improve standard of living.

Reference

Christensen, C.M. 1997. The innovator's dilemma. Cambridge, MA: Harvard Business School Press.

Connecting Dots

Gray Grantham: You want to talk about the brief?

Darby Shaw: Everyone I have told about the brief is dead.

Gray Grantham: I'll take my chances.

--The Pelican Brief

Murray Rothbard once observed that people often fail to grasp the context in which politicians make their decisions. People seem to figure that policians were just dipped into political office temporarily, and that the background context before, during, and after their office tenure doesn't matter much.

Rothbard thought that it mattered a ton. Indeed, one of his greatest strengths was tracing the connections of public figures to special interests who want to influence the market for political favor. He masterfully connects the people involved in the development of the Federal Reserve to the interests of the bankers in his History of Money and Banking in the United States.

He does so again to explain the influence of the Morgan and Rockefeller interests in the advent of world war. Hard not to raise an eyebrow or two when you see how densely populated public offices were with reps from these two camps.

Darby Shaw: Everyone I have told about the brief is dead.

Gray Grantham: I'll take my chances.

--The Pelican Brief

Murray Rothbard once observed that people often fail to grasp the context in which politicians make their decisions. People seem to figure that policians were just dipped into political office temporarily, and that the background context before, during, and after their office tenure doesn't matter much.

Rothbard thought that it mattered a ton. Indeed, one of his greatest strengths was tracing the connections of public figures to special interests who want to influence the market for political favor. He masterfully connects the people involved in the development of the Federal Reserve to the interests of the bankers in his History of Money and Banking in the United States.

He does so again to explain the influence of the Morgan and Rockefeller interests in the advent of world war. Hard not to raise an eyebrow or two when you see how densely populated public offices were with reps from these two camps.

Tuesday, September 20, 2011

Tears of the Sun

Acting on your best behavior

Turn your back on Mother Nature

Everybody wants to rule the world

--Tears for Fears

The Solyndra news demonstrates several problems associated with central planning. A week or so back Solyndra, a manufacturer of cylindrical solar panels for rooftops, filed for bankruptcy. In and of itself this is not unusual, as companies go bankrupt every day. In this case, unfortunately, the company had been the recipient of more than half a billion dollars in guaranteed loans as part of federal government programs targeting more alternative energy production.

What we have here is a default with US citizens out a cool $500 million.

In addition, there is growing evidence that Obama administration officials rushed the loan process in order to squeeze it into the 2009 federal stimulus package. It is also apparent that government controls did not provide adequate early warning signals. Indeed, program backers in Congress voiced surprise at the bankruptcy, claiming that the company told them that 'things were looking better' just two months back.

When the federal government takes money out of private hands and 'invests' it in a tech startup like Solyndra, it is basically saying that it knows how to allocate capital better than private investors. The absurdity of this propostion cannot be overstated.

In unhampered (free) market systems, capital is privately owned and controlled. The governing mechanism in private investment decisions is the economic assessment of risk vs reward. Projects with risk:reward profiles that are deemed favorable attract capital; those with unattractive profiles are shunned. 'Good' investments are rewarded with a positive return; 'bad' investments are penalized with material loss.

In contrast, the federal government's Alt E investment portfolio (which currently amounts to about $40 billion) represents a socialistic design. Property and decision-making control are in the hands of bureaucrats rather than private citizens. In this situation, it is the job of the planning bureau to allocate capital. But what precisely is the mechanism governing decision-making here? It obviously is not the economic risk:reward assessment governing private investment decisions. After all, the $500 million Solyndra loss is not coming out of the planners' pockets.

The governing mechanism of socialistic planning decisions is one of political economy. When bureaucrats have the power to allocate resources, a market is made for political favor. Politicians trade those resources in exchange for support from special interest groups (SIGs). Rather than assessing risk of capital loss, politicians assess risk of office loss, or the loss of power that comes with political office.

Clearly the different governing mechanisms will lead to different allocation decisions. An investment in Alt E deemed as unattractive to private investors may appear attractive to bureaucrats if it wins favor from SIGs who, for example, dream of a world built on 'green' technology.

The problem, of course, is that real economic resources are more likely to be squandered in unproductive projects. General standard of living is likely to fall when government gets involved in 'investing.'

The other issue raised by the Solyndra story is the government's chronic deficiency as a regulator. Lacking economic incentive, government controls are unlikely to detect problems early if at all. In contrast, private investors are highly motivated to construct sophisticated information systems that permit routine monitoring of investment projects.

The irony is that, although oversight is often viewed as a principal role of government, poor control systems are apt to result in regulatory failure. The Solyndra case is but one small example of regulatory failure that we witness time and time again.

The proper role of government is to help people protect their life, liberty, and property. When it violates those limits, government hinders, rather than advances, general standard of living.

The Solyndra case reflects the fractal nature of the general problem.

Turn your back on Mother Nature

Everybody wants to rule the world

--Tears for Fears

The Solyndra news demonstrates several problems associated with central planning. A week or so back Solyndra, a manufacturer of cylindrical solar panels for rooftops, filed for bankruptcy. In and of itself this is not unusual, as companies go bankrupt every day. In this case, unfortunately, the company had been the recipient of more than half a billion dollars in guaranteed loans as part of federal government programs targeting more alternative energy production.

What we have here is a default with US citizens out a cool $500 million.

In addition, there is growing evidence that Obama administration officials rushed the loan process in order to squeeze it into the 2009 federal stimulus package. It is also apparent that government controls did not provide adequate early warning signals. Indeed, program backers in Congress voiced surprise at the bankruptcy, claiming that the company told them that 'things were looking better' just two months back.

When the federal government takes money out of private hands and 'invests' it in a tech startup like Solyndra, it is basically saying that it knows how to allocate capital better than private investors. The absurdity of this propostion cannot be overstated.

In unhampered (free) market systems, capital is privately owned and controlled. The governing mechanism in private investment decisions is the economic assessment of risk vs reward. Projects with risk:reward profiles that are deemed favorable attract capital; those with unattractive profiles are shunned. 'Good' investments are rewarded with a positive return; 'bad' investments are penalized with material loss.

In contrast, the federal government's Alt E investment portfolio (which currently amounts to about $40 billion) represents a socialistic design. Property and decision-making control are in the hands of bureaucrats rather than private citizens. In this situation, it is the job of the planning bureau to allocate capital. But what precisely is the mechanism governing decision-making here? It obviously is not the economic risk:reward assessment governing private investment decisions. After all, the $500 million Solyndra loss is not coming out of the planners' pockets.

The governing mechanism of socialistic planning decisions is one of political economy. When bureaucrats have the power to allocate resources, a market is made for political favor. Politicians trade those resources in exchange for support from special interest groups (SIGs). Rather than assessing risk of capital loss, politicians assess risk of office loss, or the loss of power that comes with political office.

Clearly the different governing mechanisms will lead to different allocation decisions. An investment in Alt E deemed as unattractive to private investors may appear attractive to bureaucrats if it wins favor from SIGs who, for example, dream of a world built on 'green' technology.

The problem, of course, is that real economic resources are more likely to be squandered in unproductive projects. General standard of living is likely to fall when government gets involved in 'investing.'

The other issue raised by the Solyndra story is the government's chronic deficiency as a regulator. Lacking economic incentive, government controls are unlikely to detect problems early if at all. In contrast, private investors are highly motivated to construct sophisticated information systems that permit routine monitoring of investment projects.

The irony is that, although oversight is often viewed as a principal role of government, poor control systems are apt to result in regulatory failure. The Solyndra case is but one small example of regulatory failure that we witness time and time again.

The proper role of government is to help people protect their life, liberty, and property. When it violates those limits, government hinders, rather than advances, general standard of living.

The Solyndra case reflects the fractal nature of the general problem.

Hedge Hog

Here come the man

With the look in his eye

Fed on nothing

But full of pride

--INXS

As a result of today's MSFT sale, I am pretty much flat risky assets on a net basis. Long positions in Cisco (CSCO) and ag commodities (RJA) are offset by a short position in SPX (SH).

A fully hedged position feels good ahead of the Fed's special two day soiree which is setting up as a binary event.

If the Fed injects another round of drugs and markets trip higher, then I hope to unload some of my CSCO exposure. If the Fed takes the narcotics away and markets head into withdrawal, then I might trim my short book. Either way, chances are that my risk will be pretty manageable.

My sense is that the Fed may in fact do nothing--with the justification that it is already propping up Euro banks. Why nothing from a central bank that loves to meddle? It is becoming politically less palatable to engage in interventionary behavior. Plus, the marginal bang for each interventionary buck is approaching the zero bound.

If the Fed does indeed stand pat, then domestic markets will likely fall thru the floor.

position in CSCO, RJA, SH

With the look in his eye

Fed on nothing

But full of pride

--INXS

As a result of today's MSFT sale, I am pretty much flat risky assets on a net basis. Long positions in Cisco (CSCO) and ag commodities (RJA) are offset by a short position in SPX (SH).

A fully hedged position feels good ahead of the Fed's special two day soiree which is setting up as a binary event.

If the Fed injects another round of drugs and markets trip higher, then I hope to unload some of my CSCO exposure. If the Fed takes the narcotics away and markets head into withdrawal, then I might trim my short book. Either way, chances are that my risk will be pretty manageable.

My sense is that the Fed may in fact do nothing--with the justification that it is already propping up Euro banks. Why nothing from a central bank that loves to meddle? It is becoming politically less palatable to engage in interventionary behavior. Plus, the marginal bang for each interventionary buck is approaching the zero bound.

If the Fed does indeed stand pat, then domestic markets will likely fall thru the floor.

position in CSCO, RJA, SH

Microsoft Sold

Once I ran to you

Now I'll run from you

--Soft Cell

Unloaded my Microsoft (MSFT) position into this morning's lift. This position was built ahead of the signing of the debt deal. MSFT was trading well in a drekky tape and the thesis was that any relief rally would find MSFT leading the way higher.

Instead, the debt deal was met with a nasty sell off, and renewed probs in the EU opened the trap doors. MSFT went down the drain w/ the tape. Important lesson: a stock can trade great...until it doesn't...

After lugging this position thru the morass of the past two months, I feel fortunate to have salvaged a profitable shekel or two on the trade.

MSFT is now back up to where is was before the collapse. Can it go higher? Fer shure, dude. But resistance looms directly above, and to me there's more downside than upside in the name.

Although I became bullish on MSFT on a valuation basis early in the year, I have revised my view given the darkening macro context. That context has me thinking that MSFT is no great value here, since a slower economy may drag cash flows significantly lower.

MSFT's current enterprise value is about $190 billion. My interest will be rekindled if EV reaches gets down to the $120-130 zone, or 1/3 off the current price.

no positions

Now I'll run from you

--Soft Cell

Unloaded my Microsoft (MSFT) position into this morning's lift. This position was built ahead of the signing of the debt deal. MSFT was trading well in a drekky tape and the thesis was that any relief rally would find MSFT leading the way higher.

Instead, the debt deal was met with a nasty sell off, and renewed probs in the EU opened the trap doors. MSFT went down the drain w/ the tape. Important lesson: a stock can trade great...until it doesn't...

After lugging this position thru the morass of the past two months, I feel fortunate to have salvaged a profitable shekel or two on the trade.

MSFT is now back up to where is was before the collapse. Can it go higher? Fer shure, dude. But resistance looms directly above, and to me there's more downside than upside in the name.

Although I became bullish on MSFT on a valuation basis early in the year, I have revised my view given the darkening macro context. That context has me thinking that MSFT is no great value here, since a slower economy may drag cash flows significantly lower.

MSFT's current enterprise value is about $190 billion. My interest will be rekindled if EV reaches gets down to the $120-130 zone, or 1/3 off the current price.

no positions

Monday, September 19, 2011

You No Longer Own It, WE Do

"As long as there's no find, the noble brotherhood will last. But when the piles of gold begin to grow...that's when the trouble starts."

--Howard (The Treasure of the Sierra Madre)

Venzuela is nationalizing its gold industry. This is one of the big risks with owning natural resource companies in general and precious metals miners in particular.

Political risk looms large in this sector.

On the other hand, the physical commodity itself does not carry political risk--at least of the kind that amounts to expropriation of producer property.

position in gold

--Howard (The Treasure of the Sierra Madre)

Venzuela is nationalizing its gold industry. This is one of the big risks with owning natural resource companies in general and precious metals miners in particular.

Political risk looms large in this sector.

On the other hand, the physical commodity itself does not carry political risk--at least of the kind that amounts to expropriation of producer property.

position in gold

German Thumbs Down

Here comes the rain again

Falling on my head like a memory

Falling on my head like a new emotion

--Eurythmics

Over the weekend,German Chancellor Angela Merkel's party was defeated in a Berlin state election. The defeat casts doubt on continued German support of EU bailouts.

Germany is the 'have' while nearly all of the the other EU countries are 'have nots.' The multi-trillion dollar question is whether the haves are willing to bail out those who have acted imprudently.

These election results suggest that the answer to that question is 'no.'

Markets are off sigificantly this am.

position in SPX

Falling on my head like a memory

Falling on my head like a new emotion

--Eurythmics

Over the weekend,German Chancellor Angela Merkel's party was defeated in a Berlin state election. The defeat casts doubt on continued German support of EU bailouts.

Germany is the 'have' while nearly all of the the other EU countries are 'have nots.' The multi-trillion dollar question is whether the haves are willing to bail out those who have acted imprudently.

These election results suggest that the answer to that question is 'no.'

Markets are off sigificantly this am.

position in SPX

Sunday, September 18, 2011

The Empire State

War, children yeah, it's just a shot away

It's just a shot away

--Rolling Stones

Judge N traces the history of empire-building that began w/ the Spanish American War. Millions have died and we've lost freedom.

Today we have 100+ military commitments and over 900 permanent military commitments worldwide. There can be little doubt that this raises animosity against the US worldwide. We would feed similarly if China made similar occupationists moves around the world.

An empire that occupies abroad occupies at home.

It's just a shot away

--Rolling Stones

Judge N traces the history of empire-building that began w/ the Spanish American War. Millions have died and we've lost freedom.

Today we have 100+ military commitments and over 900 permanent military commitments worldwide. There can be little doubt that this raises animosity against the US worldwide. We would feed similarly if China made similar occupationists moves around the world.

An empire that occupies abroad occupies at home.

Friday, September 16, 2011

Pyramid Power

If you want to find all the cops

They're hanging out in the donut shop

They sing and dance

Spin their clubs, cruise down the block

--The Bangles

The judge reinforces our recent observation that Rick Perry's Ponzi label for Social Security is an accurate one.

The judge deftly observes that Social Security is worse than a Ponzi scheme since people can voluntarily leave Ponzis but not SS. Indeed, it can be construed that SS is not merely a fraud but outright theft or even slavery.

In a free society, the government cannot rightfully be authorized to do something that individuals cannot do themselves. Thus, the government cannot rightfully take property from individuals since individuals cannot rightfully do that to each other.

Judge N's simple example:

Someone knocks at your door. You open it to find a man pointing a gun at you. He says, "Give me your money, I want to give it to the poor."

You rush to the phone to call the police.

You find out that...he is the police. He is here to collect your tax dollars under penalty of force.

They're hanging out in the donut shop

They sing and dance

Spin their clubs, cruise down the block

--The Bangles

The judge reinforces our recent observation that Rick Perry's Ponzi label for Social Security is an accurate one.

The judge deftly observes that Social Security is worse than a Ponzi scheme since people can voluntarily leave Ponzis but not SS. Indeed, it can be construed that SS is not merely a fraud but outright theft or even slavery.

In a free society, the government cannot rightfully be authorized to do something that individuals cannot do themselves. Thus, the government cannot rightfully take property from individuals since individuals cannot rightfully do that to each other.

Judge N's simple example:

Someone knocks at your door. You open it to find a man pointing a gun at you. He says, "Give me your money, I want to give it to the poor."

You rush to the phone to call the police.

You find out that...he is the police. He is here to collect your tax dollars under penalty of force.

US Participation in Euro TARP

I think it's time we stop, children

What's that sound

Everybody look what's going down

--Buffalo Springfield

Think of yesterday's announcement that central banks around the world will offer unlimited credit for European banks choking on sovereign debt as the Euro version of TARP. TARP, or Troubled Asset Relief Program, was the label given to the Fed's program to extend ultra credit to US banks on the verge of insolvency during the credit collapse of 2008-2009.

This is a bailout program, pure and simple. Central banks money, in this case credit money, and give it to risk takers that made poor decisions.

Euro TARP has not made big headlines in the mainstream media over the past 24 hrs. It should, though, because the Federal Reserve is part of the central bank syndicate bailing out European banks. This means that US resources are being expropriated for the gain of those in other countries.

It was bad enough that in 2008, the Fed printed money at the citizenry's cost to bail out imprudent US banks.

Now, however, the Fed is printing money at the citizenry's cost to bail out imprudent bankers of other countries. On what authority is the Fed authorized to take property from US citizens for the benefit of other countries?

Any journalists that can connect a few dots should be all over this story. That the press is largely silent here suggests either severe financial illiteracy or severe bias in favor of what is plainly an unconstitutional participation of the US in Euro TARP.

What's that sound

Everybody look what's going down

--Buffalo Springfield

Think of yesterday's announcement that central banks around the world will offer unlimited credit for European banks choking on sovereign debt as the Euro version of TARP. TARP, or Troubled Asset Relief Program, was the label given to the Fed's program to extend ultra credit to US banks on the verge of insolvency during the credit collapse of 2008-2009.

This is a bailout program, pure and simple. Central banks money, in this case credit money, and give it to risk takers that made poor decisions.

Euro TARP has not made big headlines in the mainstream media over the past 24 hrs. It should, though, because the Federal Reserve is part of the central bank syndicate bailing out European banks. This means that US resources are being expropriated for the gain of those in other countries.

It was bad enough that in 2008, the Fed printed money at the citizenry's cost to bail out imprudent US banks.

Now, however, the Fed is printing money at the citizenry's cost to bail out imprudent bankers of other countries. On what authority is the Fed authorized to take property from US citizens for the benefit of other countries?

Any journalists that can connect a few dots should be all over this story. That the press is largely silent here suggests either severe financial illiteracy or severe bias in favor of what is plainly an unconstitutional participation of the US in Euro TARP.

Thursday, September 15, 2011

Cental Banks to the EU Rescue

"Do you hear that Mr Anderson? That is the sound of inevitability."

--Agent Smith (The Matrix)

This morning, a 'syndicate' of central banks stepped in to promise loans to European banks that are having trouble staying solvent. The announcement sent markets higher world wide. Euro bank stocks ripped 8-10% on the news.

The situation is similar to late 2008 when the Fed opened the uber cheap credit window to crippled US banks. Ironically, today is the third anniversary of the Lehman collapse.

Initiation of yet another bail out has stock buyers giddy today as morale hazard takes control. However, when market participants pause to consider just how dire the situation must be to motivate coordinated central bank intervention, perhaps their mood will change.

position in SPX

--Agent Smith (The Matrix)

This morning, a 'syndicate' of central banks stepped in to promise loans to European banks that are having trouble staying solvent. The announcement sent markets higher world wide. Euro bank stocks ripped 8-10% on the news.

The situation is similar to late 2008 when the Fed opened the uber cheap credit window to crippled US banks. Ironically, today is the third anniversary of the Lehman collapse.

Initiation of yet another bail out has stock buyers giddy today as morale hazard takes control. However, when market participants pause to consider just how dire the situation must be to motivate coordinated central bank intervention, perhaps their mood will change.

position in SPX

Wednesday, September 14, 2011

A Stronger CSCO

Just a little more time is all we're asking for

'Cause just a little more time can open closing doors

--Corey Hart

Cisco (CSCO) has been trading with relative strength of late. Traders seem to be perking up to this. A couple opined that perhaps CSCO is about to break its year long downtrend.

Chartgazing suggests that we're still a buck away from such an event. The downtrend line and the 50 day moving average are tracking almost exactly right now.

Am currently carrying a pretty sizable CSCO position. In past posts I have laid out the fundamental and valuation thesis that has made me bullish. The last couple of months, however, have brought me visions of 2008, where even stocks of good value are likely to be sold if we encounter a broad deleveraging event. I assign the chances of this scenario as pretty good over the next few months.

As such, I plan to lighten my CSCO position into strength. Should CSCO approach that $17.50ish area, I'll be making significant sales.

position in CSCO

'Cause just a little more time can open closing doors

--Corey Hart

Cisco (CSCO) has been trading with relative strength of late. Traders seem to be perking up to this. A couple opined that perhaps CSCO is about to break its year long downtrend.

Chartgazing suggests that we're still a buck away from such an event. The downtrend line and the 50 day moving average are tracking almost exactly right now.

Am currently carrying a pretty sizable CSCO position. In past posts I have laid out the fundamental and valuation thesis that has made me bullish. The last couple of months, however, have brought me visions of 2008, where even stocks of good value are likely to be sold if we encounter a broad deleveraging event. I assign the chances of this scenario as pretty good over the next few months.

As such, I plan to lighten my CSCO position into strength. Should CSCO approach that $17.50ish area, I'll be making significant sales.

position in CSCO

Warfare State Debate

We'll be fighting in the streets with our children at our feet

And the morals that we worshipped will be gone

And the men who spurred us on sit in judgment of all wrong

They decide and the shotgun sings the song

--The Who

Yesterday on his radio show, Glenn Beck ripped Ron Paul's performance during the preceding night's presidential candidate debate. He labeled Paul the 'biggest loser' of the debate.

While Beck agrees with Ron Paul's stance on the economy, welfare, and personal responsibility, he is at odds w/ RP on foreign policy, claiming that Paul is 'totally wrong' on his minimalist stance wrt the military.