C.K. Dexter Haven: Sometimes, for your own sake, Red, I think you should have stuck to me longer.

Tracy Lord: I thought it was for life, but the nice judge gave me a pardon.

C.K. Dexter Haven: Aahh. that's the old redhead. No bitterness. No recrimination. Just a good swift left to the jaw.

--The Philadelphia Story

Strong words taken from Justice Scalia's dissenting opinion of the Supreme Court's DOMA decision earlier this week. His main point is that the Court does not have standing in this case. The question of the legality of gay marriage is one for the states, not for the Court, to decide.

He makes a good point. And I am sympathetic to federalism arguments.

But the complicating factor here is that government is currently an originator of marriage contracts. If government is involved by law, then there is an argument to be made that equal protection applies.

This is the problem that should be addressed. Government is involved in writing marriage contracts, an endeavor in which it has no lawful business. Marriage is a contract between individuals. It is a private agreement. Government's role is to see that such contracts are enforced and to protect against fraud. It has no business brokering marriage contracts.

To truly 'let the people decide' as Justice Scalia argues, remove government from the marriage contract origination business.

Sunday, June 30, 2013

Saturday, June 29, 2013

Liberty and The Young

Another night in any town

You can hear the thunder of their cry

Ahead of their time

They wonder why

--Journey

Jacob Hornberger aims this discussion at the young. He observes that there are crises everywhere--social security, health care, immigration, war on drugs, terrorism, dollar, government spending, debt.

Early in school we are told that we live in a free country. We are also told that these crises are consequences of living in a free society.

But we do not live in a free society. The crises we face have nothing to do with living in a free society.

Instead, they have everything to do with living in a society that is increasingly controlled by central authority. Government's primary role has evolved into taking money from those to whom it belongs and giving it to those to whom it does not belong.

Hornberger observes that this is part of one of the oldest rackets in history. Concoct a threat (terrorism, poverty, drugs, etc) and convince people to surrender their liberty.

Some who understand this suggest that the best way to make progress is thru compromise. Gradually negotiate terms in the right direction and, over time, we'll be free.

But compromise requires ceding freedom. The Three Fifths clause classically demonstrates the danger of compromise. Why give up what is yours by right?

The correct approach is to seek the total dismantling of the welfare and warfare state. Only this will end the various 'crises' we face.

Younger generations must drive this repeal. Older generations have already chosen socialism and militarism and are unlikely to give sufficient ground at this point.

But older generation can not bind the young into accepting their choices. Young people can choose differently. They can choose liberty and free markets.

This is an excellent missive by JH that I plan to share with s many young people as possible.

You can hear the thunder of their cry

Ahead of their time

They wonder why

--Journey

Jacob Hornberger aims this discussion at the young. He observes that there are crises everywhere--social security, health care, immigration, war on drugs, terrorism, dollar, government spending, debt.

Early in school we are told that we live in a free country. We are also told that these crises are consequences of living in a free society.

But we do not live in a free society. The crises we face have nothing to do with living in a free society.

Instead, they have everything to do with living in a society that is increasingly controlled by central authority. Government's primary role has evolved into taking money from those to whom it belongs and giving it to those to whom it does not belong.

Hornberger observes that this is part of one of the oldest rackets in history. Concoct a threat (terrorism, poverty, drugs, etc) and convince people to surrender their liberty.

Some who understand this suggest that the best way to make progress is thru compromise. Gradually negotiate terms in the right direction and, over time, we'll be free.

But compromise requires ceding freedom. The Three Fifths clause classically demonstrates the danger of compromise. Why give up what is yours by right?

The correct approach is to seek the total dismantling of the welfare and warfare state. Only this will end the various 'crises' we face.

Younger generations must drive this repeal. Older generations have already chosen socialism and militarism and are unlikely to give sufficient ground at this point.

But older generation can not bind the young into accepting their choices. Young people can choose differently. They can choose liberty and free markets.

This is an excellent missive by JH that I plan to share with s many young people as possible.

Friday, June 28, 2013

Obamacare One Year Later

This wouldn't be the first time

Things have gone astray

Now you've thrown it all away

--Bryan Adams

Rand Paul observes that, one year after the Supreme Court ruling, Obamacare remains as unconstitutional and as opposed to natural rights as it was when 5 judges legitimized it. We have discussed many aspects of the flawed SC decision, from Chief Justice Robert's tortured opinion to institutional pressures to rule how the majority did to the ruling's lack of judicial restraint.

RP also notes the increasingly visible negative consequences of Obamacare as it approaches full implementation. These consequences were a layup to predict and will only intensify with implementation of the ACA.

As people feel the sting of these consequences, public opinion about Obamacare is turning south as well. Hopefully, this exerts enough political pressure on lawmakers to reverse one of the worst laws ever legitimized in American history.

Things have gone astray

Now you've thrown it all away

--Bryan Adams

Rand Paul observes that, one year after the Supreme Court ruling, Obamacare remains as unconstitutional and as opposed to natural rights as it was when 5 judges legitimized it. We have discussed many aspects of the flawed SC decision, from Chief Justice Robert's tortured opinion to institutional pressures to rule how the majority did to the ruling's lack of judicial restraint.

RP also notes the increasingly visible negative consequences of Obamacare as it approaches full implementation. These consequences were a layup to predict and will only intensify with implementation of the ACA.

As people feel the sting of these consequences, public opinion about Obamacare is turning south as well. Hopefully, this exerts enough political pressure on lawmakers to reverse one of the worst laws ever legitimized in American history.

Thursday, June 27, 2013

Government Programs and the Economic Scoreboard

"We're draggin' baby."

--Swamp Thing (Con Air)

Many proponents of Big Government tend to ignore the economic ramifications of their policies. It is for the common good, they say. The cost doesn't matter.

If only the world conformed to such a fairy tale. The reality is that resources are scarce, and scarcity can only be alleviated via efficient production of goods that consumers want. Policies that discourage production, or that encourage production of goods that consumers do not want, or that encourage production in manners that consume more resources than they produce, are all bound to lower general standard of living over time.

Take, for instance, welfare programs. Proponents argue that welfare programs help people when they are down and encourage them to get back on their feet and become productive. If this were true, then welfare programs should produce positive economic returns over time. Productivity should go up, and welfare programs would essentially fund themselves over time.

But they don't. Welfare programs consume more resources than they produce. Resources must be taken from producers in order to fund these programs. And they must be taken in ever greater quantities. The quantities that must be taken have become so large that we must borrow from the future to pay for them.

Government is a consumer, not a producer, of resources. All government programs carry an economic cost, some higher than others. The idea that they are an 'investment' is ludicrous, as the economic scoreboard clearly indicates that these programs generate negative returns.

They serve as a drag on progress.

--Swamp Thing (Con Air)

Many proponents of Big Government tend to ignore the economic ramifications of their policies. It is for the common good, they say. The cost doesn't matter.

If only the world conformed to such a fairy tale. The reality is that resources are scarce, and scarcity can only be alleviated via efficient production of goods that consumers want. Policies that discourage production, or that encourage production of goods that consumers do not want, or that encourage production in manners that consume more resources than they produce, are all bound to lower general standard of living over time.

Take, for instance, welfare programs. Proponents argue that welfare programs help people when they are down and encourage them to get back on their feet and become productive. If this were true, then welfare programs should produce positive economic returns over time. Productivity should go up, and welfare programs would essentially fund themselves over time.

But they don't. Welfare programs consume more resources than they produce. Resources must be taken from producers in order to fund these programs. And they must be taken in ever greater quantities. The quantities that must be taken have become so large that we must borrow from the future to pay for them.

Government is a consumer, not a producer, of resources. All government programs carry an economic cost, some higher than others. The idea that they are an 'investment' is ludicrous, as the economic scoreboard clearly indicates that these programs generate negative returns.

They serve as a drag on progress.

Wednesday, June 26, 2013

Socialism is Slavery

Morpheus: It's the world that has been pulled over your eyes to blind you from the truth.

Neo: What truth?

Morpheus: That you are a slave, Neo. Like everyone else you were born into bondage. Into a prison that you cannot taste or see or touch. A prison for your mind.

--The Matrix

Nice review by Henry Hazlitt of a work by Herbert Spencer written in 1884 called The Man Versus the State. Despite 'common wisdom' that Big Government was a product of the Progressive Era and the Great Depression, Spencer demonstrated that many statist programs (e.g., Social Security, State ownership of enterprises, escalating regulation, progressive income tax) were in motion and/or fully predictatble in the 1880s.

Spencer also notes that the meaning of liberal was already being co-opted by 'New Tories' sympathetic to State interventionism.

Spencer was clearly concerned about the ramifications of socialism on freedom. Marx and Engel's work had revived socialist movements, which were active in Europe and in the US by the late 1800s.

I wanted to record Spencer's comments on socialism and slavery:

"All socialism...involves slavery. That which fundamentally distinguishes the slave is that he labors under coercion to satisfy another's desires." Taxation is thus a form of slavery of the individual to the community. "Essential question is - How much is he compelled to labor for other benefit than his own, and how much can he labor for his own benefit?"

Spencer titles an early chapter "The Coming Slavery."

The future is now.

Neo: What truth?

Morpheus: That you are a slave, Neo. Like everyone else you were born into bondage. Into a prison that you cannot taste or see or touch. A prison for your mind.

--The Matrix

Nice review by Henry Hazlitt of a work by Herbert Spencer written in 1884 called The Man Versus the State. Despite 'common wisdom' that Big Government was a product of the Progressive Era and the Great Depression, Spencer demonstrated that many statist programs (e.g., Social Security, State ownership of enterprises, escalating regulation, progressive income tax) were in motion and/or fully predictatble in the 1880s.

Spencer also notes that the meaning of liberal was already being co-opted by 'New Tories' sympathetic to State interventionism.

Spencer was clearly concerned about the ramifications of socialism on freedom. Marx and Engel's work had revived socialist movements, which were active in Europe and in the US by the late 1800s.

I wanted to record Spencer's comments on socialism and slavery:

"All socialism...involves slavery. That which fundamentally distinguishes the slave is that he labors under coercion to satisfy another's desires." Taxation is thus a form of slavery of the individual to the community. "Essential question is - How much is he compelled to labor for other benefit than his own, and how much can he labor for his own benefit?"

Spencer titles an early chapter "The Coming Slavery."

The future is now.

Tuesday, June 25, 2013

Cash as a Scarce Asset

Money's too tight to mention

--Simply Red

Peter Atwater makes the case that cash is the most underinvested asset class out there. Low cash positions in stock and bond mutual funds and ETFs are at about 20% of total assets. In 1982 they were more than 80%.

Low fund cash levels refute the notion that there's lots of cash 'on the sidelines' waiting to be put to work.

Atwater also thinks that it is unlikely that money comes out of bonds and into stocks because lower bond prices (like we're seeing) motivate redemptions, and bond funds often hold illiquid instruments--meaning that funds will need extra cash for redemption purposes.

He wonders whether the more likely scenario is one where stocks and bonds both fall while cash balances rise. Note that this missive is about two weeks old and we have since seen precisely this.

Tell people that you are holding lots of cash and you're likely to be the subject of ridicule, suggests Peter. This zero rate environment has conditioned people to believe that 'cash is trash.' You need to trade out of your cash to get some yield or to protect your purchasing power from being destroyed by the monetary printing press.

After being biased toward deflationary resolution to this situation and a high cash balance , I've admittedly become more sympathetic to the inflationary cash is trash argument myself.

One reason is that it is seems increasingly clear that policymakers will not pick up their toys and go home in the event of another correlated price decline a la 2008. They will go all in. This means circumventing the 'credit money' system and sending money to people in boxes (or electronically to their banking accounts as the case may be).

So although cash may be a scarce asset out there (per Peter Atwater), central banks could easily make it as common as air. This to me seems the likely endgame--even if in the interim we get another whiff of deflation where cash is dear.

Regardless of whether you lean toward inflationary or deflationary resolution, we are in the midst of financial oppression. All scenarios lead to ugly outcomes.

--Simply Red

Peter Atwater makes the case that cash is the most underinvested asset class out there. Low cash positions in stock and bond mutual funds and ETFs are at about 20% of total assets. In 1982 they were more than 80%.

Low fund cash levels refute the notion that there's lots of cash 'on the sidelines' waiting to be put to work.

Atwater also thinks that it is unlikely that money comes out of bonds and into stocks because lower bond prices (like we're seeing) motivate redemptions, and bond funds often hold illiquid instruments--meaning that funds will need extra cash for redemption purposes.

He wonders whether the more likely scenario is one where stocks and bonds both fall while cash balances rise. Note that this missive is about two weeks old and we have since seen precisely this.

Tell people that you are holding lots of cash and you're likely to be the subject of ridicule, suggests Peter. This zero rate environment has conditioned people to believe that 'cash is trash.' You need to trade out of your cash to get some yield or to protect your purchasing power from being destroyed by the monetary printing press.

After being biased toward deflationary resolution to this situation and a high cash balance , I've admittedly become more sympathetic to the inflationary cash is trash argument myself.

One reason is that it is seems increasingly clear that policymakers will not pick up their toys and go home in the event of another correlated price decline a la 2008. They will go all in. This means circumventing the 'credit money' system and sending money to people in boxes (or electronically to their banking accounts as the case may be).

So although cash may be a scarce asset out there (per Peter Atwater), central banks could easily make it as common as air. This to me seems the likely endgame--even if in the interim we get another whiff of deflation where cash is dear.

Regardless of whether you lean toward inflationary or deflationary resolution, we are in the midst of financial oppression. All scenarios lead to ugly outcomes.

Monday, June 24, 2013

Spy Squared

"Don't look up. You're on Candid Camera."

--James Bond (The Spy Who Loved Me)

The federal government has now charged NSA whistleblower Edward Snowden with espionage. So, we now have a government that has been spying on its own people accusing a citizen of spying on the people when he revealed the program.

You can't make this stuff up.

--James Bond (The Spy Who Loved Me)

The federal government has now charged NSA whistleblower Edward Snowden with espionage. So, we now have a government that has been spying on its own people accusing a citizen of spying on the people when he revealed the program.

You can't make this stuff up.

How Much Leverage Is In Treasuries?

"The mother of all evils is speculation - leveraged debt."

--Gordon Gekko (Wall Street: Money Never Sleeps)

Ten yr rates flying again this morning. Stock down in sympathy about 1.5%.

In a zero interest rate policy (ZIRP) world with investors reaching for yield, are we under-estimating how much leverage is in Treasuries? There is a case to be made that investors are leveraged long Treasuries at historic proportions.

If so, and those carry traders are becoming risk averse, then selling begets selling. And dominos fall.

position in SPX, Treasuries

--Gordon Gekko (Wall Street: Money Never Sleeps)

Ten yr rates flying again this morning. Stock down in sympathy about 1.5%.

In a zero interest rate policy (ZIRP) world with investors reaching for yield, are we under-estimating how much leverage is in Treasuries? There is a case to be made that investors are leveraged long Treasuries at historic proportions.

If so, and those carry traders are becoming risk averse, then selling begets selling. And dominos fall.

position in SPX, Treasuries

Sunday, June 23, 2013

NSA and the Fourth Amendment

I'll get all my papers and I smile at the sky

Though I know that the hypnotized never lie

--The Who

Proponents of NSA tracking of phone calls in the US, along with other government spying programs on American citizens, put forth various arguments. The technology makes it easy to do. It's a small price to pay to be safe from terrorists. The Patriot Act makes it legal.

But it is not legal. The Fourth Amendment states:

"The right of the people to be secure in their persons, houses, papers, and effects, against unreasonable searches and seizures, shall not be violated, and no Warrants shall issue, but upon probable cause, supported by Oath or affirmation, and particularly describing the place to be searched, and the persons or things to be seized."

The Constitution is clear. People have to the right to be secure in their person and possessions against search and seizure by government. If government wants to search or seize, then a warrant must be issued by a judicial authority. To be valid, a warrant must be specific in terms of where a search is to take place, and what is to be seized.

There are no provisions for standing or blanket search warrants such as those being authorized by FISA courts, nor are there exceptions for cases of 'national security.'

An federal government program that takes records from private hands over a period of time with a stated purpose of monitoring potential terrorist activity is clearly unconstitutional.

Full-throated debate about the trade-off between safety and freedom is welcome and long overdue. But the Constitution is clear, and it is wholly consistent with natural law.

If this law is to be changed, then that change must follow the law as well--in the form of the amendment process to the Constitution. Statists face an uphill battle in that regard.

Though I know that the hypnotized never lie

--The Who

Proponents of NSA tracking of phone calls in the US, along with other government spying programs on American citizens, put forth various arguments. The technology makes it easy to do. It's a small price to pay to be safe from terrorists. The Patriot Act makes it legal.

But it is not legal. The Fourth Amendment states:

"The right of the people to be secure in their persons, houses, papers, and effects, against unreasonable searches and seizures, shall not be violated, and no Warrants shall issue, but upon probable cause, supported by Oath or affirmation, and particularly describing the place to be searched, and the persons or things to be seized."

The Constitution is clear. People have to the right to be secure in their person and possessions against search and seizure by government. If government wants to search or seize, then a warrant must be issued by a judicial authority. To be valid, a warrant must be specific in terms of where a search is to take place, and what is to be seized.

There are no provisions for standing or blanket search warrants such as those being authorized by FISA courts, nor are there exceptions for cases of 'national security.'

An federal government program that takes records from private hands over a period of time with a stated purpose of monitoring potential terrorist activity is clearly unconstitutional.

Full-throated debate about the trade-off between safety and freedom is welcome and long overdue. But the Constitution is clear, and it is wholly consistent with natural law.

If this law is to be changed, then that change must follow the law as well--in the form of the amendment process to the Constitution. Statists face an uphill battle in that regard.

Saturday, June 22, 2013

Libertarianism and Fearful Statists

"If I have a fault, it's candor."

--Rafe McCawley (Pearl Harbor)

To the question of why hasn't libertarianism won the day, Jacob Hornberger offers a direct answer. Many, if not most people, are statists. Statists do not want to be free to manage their lives and be responsible for their actions. They want the government to take care of them and to keep them safe.

They are ok with the strong arm of government taking resources from some and giving those resources to others. Statists do not see anything wrong with the process--as long as it is the government doing the taking and the redistributing. It is a way of getting more for less without breaking the law.

Hornberger posits that many statists live in fear--of starving, of dying from disease, of terrorists, of communists, of illegal aliens, etc. Consistent with the tenets of threat-rigidity theory, statists are willing to centralize decision-making authority to the federal government in order to cope with their fears.

Hornberger observes the folly of giving up freedom for security. As Benjamin Franklin, Patrick Henry, and others astutely observed long ago, trading freedom for security results in neither over time. Government, with its insatiable appetite for power, assumes ever more control.

Progress is made under conditions of freedom, where people act in manners to advance their interests, standard of living declines when people cede liberty to government.

Understandably, a growing fear of statists is this: the ranks of libertarians, those people who want to dismantle the welfare and warfare state in favor of freedom, are growing by the day.

--Rafe McCawley (Pearl Harbor)

To the question of why hasn't libertarianism won the day, Jacob Hornberger offers a direct answer. Many, if not most people, are statists. Statists do not want to be free to manage their lives and be responsible for their actions. They want the government to take care of them and to keep them safe.

They are ok with the strong arm of government taking resources from some and giving those resources to others. Statists do not see anything wrong with the process--as long as it is the government doing the taking and the redistributing. It is a way of getting more for less without breaking the law.

Hornberger posits that many statists live in fear--of starving, of dying from disease, of terrorists, of communists, of illegal aliens, etc. Consistent with the tenets of threat-rigidity theory, statists are willing to centralize decision-making authority to the federal government in order to cope with their fears.

Hornberger observes the folly of giving up freedom for security. As Benjamin Franklin, Patrick Henry, and others astutely observed long ago, trading freedom for security results in neither over time. Government, with its insatiable appetite for power, assumes ever more control.

Progress is made under conditions of freedom, where people act in manners to advance their interests, standard of living declines when people cede liberty to government.

Understandably, a growing fear of statists is this: the ranks of libertarians, those people who want to dismantle the welfare and warfare state in favor of freedom, are growing by the day.

Friday, June 21, 2013

Looks Bearish

So glad we've almost made it

So sad they had to fade it

--Tears for Fears

Just a brief end of day note that if I were not already significantly short already, I would likely be fading (read: selling) this this relatively weak bounce in equities.

Meanwhile, Treasuries continue to get pounded. Ten year yields crossed 2.5% today and are currently at day highs. Ten year yields are now up about 50% since early May.

My trading feel recently has been awful, but it seems like cards are falling in Boo's favor here and that risk is to the downside.

position in SPX, Treasuries

So sad they had to fade it

--Tears for Fears

Just a brief end of day note that if I were not already significantly short already, I would likely be fading (read: selling) this this relatively weak bounce in equities.

Meanwhile, Treasuries continue to get pounded. Ten year yields crossed 2.5% today and are currently at day highs. Ten year yields are now up about 50% since early May.

My trading feel recently has been awful, but it seems like cards are falling in Boo's favor here and that risk is to the downside.

position in SPX, Treasuries

Psychology of Negative Consequences

"This is a pleasant fiction, is it not?"

--Lucilla (Gladiator)

Another interesting presentation and Q&A with Kyle Bass. Bass sees Japan as the first to blow from misguided monetary and fiscal policies and his fund has a significant bet in that direction. He thinks that the action in Japan markets over the past few weeks (JGBs down alongside stocks) constitute the initial tremors.

The basic thesis is that once bond markets refuse to fund profligate spending, then the party is over. We've already seen Iceland, Ireland, Greece, Cypress, et al provide a sense of what a 'funding crisis' looks like. Japan, because of its extremely ugly contex, may be the first 'big name' to come apart.

But this KB presentation was not just about Japan. I found two remarks particularly insightful. One occurs around 28 min involving the psychology of negative outcomes and the market consequences when that pyschology reverses.

What he is talking about is the psychology of denial. The biases of cognitive dissonance--overconfidence, loss aversion, endowment effect, etc--that cause people to maintain (or perhaps even escalate) a course of action even though the data suggest a change of course.

That course change always comes, but it is lagged. And when it comes, it comes quickly. Bass presents many historical examples (peso, ruble, credit crisis, Greece, etc) of the speed with which markets react. Things are ok one day and chaos the next. It happens so fast that investors cannot get out of their positions.

The interesting point that Bass makes is that much of the policy intervention has suppressed volatility--which feeds the psychology of negative outcomes to keep people from selling. But this suppression merely builds potential energy that greatly amplifies volatility when the selling commences.

We have now been in the volatility suppression phase for about 4 years. Tick tock...

The other particularly insightful remark happens at about 47 min. Bass suggests that "the central bank is the great enabler of congressional profligacy." Stated differently, without governments buying their own sovereign debt and keeping interest rates artificially low, there is no way that spending and debt would be at their current extremes.

Bass recounts that when he suggests to congresspeople that a bond crisis could result if the US keeps spending like it is, they ask KB where Treasury rates are. And when KB recites the low current rate, the congresspeople say, "We don't see a crisis."

Psychology of negative consequences writ large.

position in SPX, Treasuries

--Lucilla (Gladiator)

Another interesting presentation and Q&A with Kyle Bass. Bass sees Japan as the first to blow from misguided monetary and fiscal policies and his fund has a significant bet in that direction. He thinks that the action in Japan markets over the past few weeks (JGBs down alongside stocks) constitute the initial tremors.

The basic thesis is that once bond markets refuse to fund profligate spending, then the party is over. We've already seen Iceland, Ireland, Greece, Cypress, et al provide a sense of what a 'funding crisis' looks like. Japan, because of its extremely ugly contex, may be the first 'big name' to come apart.

But this KB presentation was not just about Japan. I found two remarks particularly insightful. One occurs around 28 min involving the psychology of negative outcomes and the market consequences when that pyschology reverses.

What he is talking about is the psychology of denial. The biases of cognitive dissonance--overconfidence, loss aversion, endowment effect, etc--that cause people to maintain (or perhaps even escalate) a course of action even though the data suggest a change of course.

That course change always comes, but it is lagged. And when it comes, it comes quickly. Bass presents many historical examples (peso, ruble, credit crisis, Greece, etc) of the speed with which markets react. Things are ok one day and chaos the next. It happens so fast that investors cannot get out of their positions.

The interesting point that Bass makes is that much of the policy intervention has suppressed volatility--which feeds the psychology of negative outcomes to keep people from selling. But this suppression merely builds potential energy that greatly amplifies volatility when the selling commences.

We have now been in the volatility suppression phase for about 4 years. Tick tock...

The other particularly insightful remark happens at about 47 min. Bass suggests that "the central bank is the great enabler of congressional profligacy." Stated differently, without governments buying their own sovereign debt and keeping interest rates artificially low, there is no way that spending and debt would be at their current extremes.

Bass recounts that when he suggests to congresspeople that a bond crisis could result if the US keeps spending like it is, they ask KB where Treasury rates are. And when KB recites the low current rate, the congresspeople say, "We don't see a crisis."

Psychology of negative consequences writ large.

position in SPX, Treasuries

Thursday, June 20, 2013

Moral Hazard Succinctly Defined

"Let me watch over you tonight."

--Claire Gregory (Someone to Watch Over Me)

A quick post to capture this nice definition of moral hazard:

"Moral hazard is the separation of risk from consequence."

About as succinct as it gets. People behave differently when they feel that they will not face negative consequences of their actions. If they perceive their behavior as being insured, then people will take more risk.

One way to visualize the transmission mechanism of the massive intervention in world markets is as an air pump that has blown a gigantic bubble in moral hazard around the globe.

--Claire Gregory (Someone to Watch Over Me)

A quick post to capture this nice definition of moral hazard:

"Moral hazard is the separation of risk from consequence."

About as succinct as it gets. People behave differently when they feel that they will not face negative consequences of their actions. If they perceive their behavior as being insured, then people will take more risk.

One way to visualize the transmission mechanism of the massive intervention in world markets is as an air pump that has blown a gigantic bubble in moral hazard around the globe.

Heavy Hand

I close my eyes

Oh God I think I'm falling

Out of the skies, I close my eyes

Heaven help me

--Madonna

The SPX wound up taking out the aforementioned 1600 support level and closed near the lows at -2.5% on big volume. The Dow was down 354. Treasuries never mustered a rally, which may be most telling.

Along with the FOMC 'tapering' thread, Greece is back on the radar with 'new' funding issues. There is also chatter that China is facing some bank insolvencies after leveraged commodity trading went the wrong way.

Will be interesting to see how markets trade overnight.

Meanwhile, it appears that the next significant level of support for the SPX lies below at 1540.

position in SPX, Treasuries

Oh God I think I'm falling

Out of the skies, I close my eyes

Heaven help me

--Madonna

The SPX wound up taking out the aforementioned 1600 support level and closed near the lows at -2.5% on big volume. The Dow was down 354. Treasuries never mustered a rally, which may be most telling.

Along with the FOMC 'tapering' thread, Greece is back on the radar with 'new' funding issues. There is also chatter that China is facing some bank insolvencies after leveraged commodity trading went the wrong way.

Will be interesting to see how markets trade overnight.

Meanwhile, it appears that the next significant level of support for the SPX lies below at 1540.

position in SPX, Treasuries

FOMC Sparks Selling

I bought a toothbrush, some toothpaste

A flannel for my face

Pajamas, a hairbrush

New shoes and a case

I said to my reflection

Let's get out of this place

--Squeeze

After chewing on yesterday's FOMC statement and Bernanke's subsequent press conference remarks, world markets decided that they didn't taste good.

Domestic markets opened red and thus far are trending lower. The SPX has cut thru the 50 day moving avg and violated the uptrend line in place since last November. Near term support at 1600 is coming up close.

Once again, Treasuries are not a beneficiary of a 'risk off' mentality. In the past, investors bought bonds when they sold stocks. Currently both are being sold--consistent with the pattern observed in Japan.

This is what the early stages of a funding crisis looks like.

Gold is selling off again--down another 3.5%.

It appears carry traders are getting squeezed as interest rates rise and prices fall.

position in SPX, Treasuries, gold

A flannel for my face

Pajamas, a hairbrush

New shoes and a case

I said to my reflection

Let's get out of this place

--Squeeze

After chewing on yesterday's FOMC statement and Bernanke's subsequent press conference remarks, world markets decided that they didn't taste good.

Domestic markets opened red and thus far are trending lower. The SPX has cut thru the 50 day moving avg and violated the uptrend line in place since last November. Near term support at 1600 is coming up close.

Once again, Treasuries are not a beneficiary of a 'risk off' mentality. In the past, investors bought bonds when they sold stocks. Currently both are being sold--consistent with the pattern observed in Japan.

This is what the early stages of a funding crisis looks like.

Gold is selling off again--down another 3.5%.

It appears carry traders are getting squeezed as interest rates rise and prices fall.

position in SPX, Treasuries, gold

Wednesday, June 19, 2013

Getting More for Less

Come on, baby, dry your eyes

Wipe your tears

Never like to see you cry

--Human League

While at Target (TGT) last weekend, I mistakenly walked out of the store with a bag of fertilizer that I didn't pay for. I had put the bag on the bottom cart rack and forgot that it was down there when I was checking out. Neither the cashier nor I noticed it.

I was still oblivious while putting the items that I did pay for into my car. It wasn't until the cart was empty that the bag on the bottom rack was visible.

Rationalizing about keeping it was easy. It's heavy and would be a hassle to take back in. I'll more than make up for this freebie with future purchases. It's the cashier's responsibility to look out for items on the bottom of the cart. It's Target's problem, not mine. This makes up for the high price I paid on that other item.

So I started home with my bag of 'free' fertilizer. That little voice inside my head got louder with each mile I drove away from the store. My conscience was yelling at me. It is wrong to take someone else's property.

About half way home, I turned the car around, went back to the store, carted the bag inside, and paid for it.

The urge to get more for less, or in its extreme form the urge to get something for nothing, is strong. It comes from the axiomatic drive in each of us to economize. Resources are scarce. In our efforts to reduce scarcity, we want to be as productive as possible. Stated more plainly, each of us wants to get as much out of life as we can. What exactly each of us desires varies from person to person. Some desire lots of material goods. Others value good feelings or spiritual benefits.

Whatever the case, we jump at the chance to get more of what we want for less cost. It drives us to take the escalator rather than the stairs, to clip coupons and shop for discounts, to buy lottery tickets, to park closer rather than farther away from our destination, to seek more pay for the same (or even less) amount of work, to constantly seek faster ways to get to where we want to go.

The problem is that our drive to economize can cause us to blur the line betwen right and wrong. Taking home that bag of fertilizer is ok because it will more than even out in the long run. Taking property from others at gunpoint is ok because it levels out wealth and some of what is taken helps the poor.

We might be led to act on this temptation, doing wrong directly through our own behavior or indirectly through the behavior of institutional agents who act on our behalf.

The urge to get more for less fosters the aggression that opposes freedom.

no positions

Wipe your tears

Never like to see you cry

--Human League

While at Target (TGT) last weekend, I mistakenly walked out of the store with a bag of fertilizer that I didn't pay for. I had put the bag on the bottom cart rack and forgot that it was down there when I was checking out. Neither the cashier nor I noticed it.

I was still oblivious while putting the items that I did pay for into my car. It wasn't until the cart was empty that the bag on the bottom rack was visible.

Rationalizing about keeping it was easy. It's heavy and would be a hassle to take back in. I'll more than make up for this freebie with future purchases. It's the cashier's responsibility to look out for items on the bottom of the cart. It's Target's problem, not mine. This makes up for the high price I paid on that other item.

So I started home with my bag of 'free' fertilizer. That little voice inside my head got louder with each mile I drove away from the store. My conscience was yelling at me. It is wrong to take someone else's property.

About half way home, I turned the car around, went back to the store, carted the bag inside, and paid for it.

The urge to get more for less, or in its extreme form the urge to get something for nothing, is strong. It comes from the axiomatic drive in each of us to economize. Resources are scarce. In our efforts to reduce scarcity, we want to be as productive as possible. Stated more plainly, each of us wants to get as much out of life as we can. What exactly each of us desires varies from person to person. Some desire lots of material goods. Others value good feelings or spiritual benefits.

Whatever the case, we jump at the chance to get more of what we want for less cost. It drives us to take the escalator rather than the stairs, to clip coupons and shop for discounts, to buy lottery tickets, to park closer rather than farther away from our destination, to seek more pay for the same (or even less) amount of work, to constantly seek faster ways to get to where we want to go.

The problem is that our drive to economize can cause us to blur the line betwen right and wrong. Taking home that bag of fertilizer is ok because it will more than even out in the long run. Taking property from others at gunpoint is ok because it levels out wealth and some of what is taken helps the poor.

We might be led to act on this temptation, doing wrong directly through our own behavior or indirectly through the behavior of institutional agents who act on our behalf.

The urge to get more for less fosters the aggression that opposes freedom.

no positions

Tuesday, June 18, 2013

Market Distortion

Once you're gone

You can't come back

When you're out of the blue

And into the black

--Neil Young

John Hussman once more emphasizes the two catogories of government policy that are massively distorting markets. Current fiscal policy encourages spending and debt. This policy distorts markets by artificially discounting the value of savings versus consumption. It also amounts to a large transfer of wealth from consumers to producers. The correlation between aggregate debt and corporate profits continues to be eye-opening to me. Corporate shareholders are the primary beneficiaries.

Monetary policy encourages further borrowing and leveraged speculation. This policy distorts markets by depleting the stock of savings even more. Meanwhile, investors seeking income must 'reach for yield' by buying risky securities that they would never touch in unhampered markets. Carry traders borrow cheaply to finance speculative projects with huge leverage.

If these policies and/or the perception of their benefits do not persist indefinitely, then a large reversal of fortune is pending.

position in SPX, Treasuries

You can't come back

When you're out of the blue

And into the black

--Neil Young

John Hussman once more emphasizes the two catogories of government policy that are massively distorting markets. Current fiscal policy encourages spending and debt. This policy distorts markets by artificially discounting the value of savings versus consumption. It also amounts to a large transfer of wealth from consumers to producers. The correlation between aggregate debt and corporate profits continues to be eye-opening to me. Corporate shareholders are the primary beneficiaries.

Monetary policy encourages further borrowing and leveraged speculation. This policy distorts markets by depleting the stock of savings even more. Meanwhile, investors seeking income must 'reach for yield' by buying risky securities that they would never touch in unhampered markets. Carry traders borrow cheaply to finance speculative projects with huge leverage.

If these policies and/or the perception of their benefits do not persist indefinitely, then a large reversal of fortune is pending.

position in SPX, Treasuries

Monday, June 17, 2013

In Government We Trust?

"Exactly right!"

--Wade Garrett (Road House)

Rand Paul discusses the intent of a group of congressmen to take legal action against the federal government for infringing on Americans' Fourth Amendment rights.

Many, including the president, have defended the recent government spying activities on the grounds that we should trust the government. However, as Paul notes,

"Our Founders never intended for Americans to trust their government. Our entire Constitution was predicated on the notion that government was a necessary evil, to be restrained and minimized as much as possible."

Precisely.

RP further observes that indiscriminate monitoring of citizens is just the kind of general warranting that we fought a revolution over. The Fourth Amendment clearly states that warrants must be specific to the person and place.

Current federal government practices feed "the inevitable arrogance of power."

In God we trust. Yes. In government we trust. No.

--Wade Garrett (Road House)

Rand Paul discusses the intent of a group of congressmen to take legal action against the federal government for infringing on Americans' Fourth Amendment rights.

Many, including the president, have defended the recent government spying activities on the grounds that we should trust the government. However, as Paul notes,

"Our Founders never intended for Americans to trust their government. Our entire Constitution was predicated on the notion that government was a necessary evil, to be restrained and minimized as much as possible."

Precisely.

RP further observes that indiscriminate monitoring of citizens is just the kind of general warranting that we fought a revolution over. The Fourth Amendment clearly states that warrants must be specific to the person and place.

Current federal government practices feed "the inevitable arrogance of power."

In God we trust. Yes. In government we trust. No.

Sunday, June 16, 2013

Oath of Hypocrisy

"Listen, I'm a politician. Which means I'm a cheat and a liar. And when I'm not kissing babies, I'm stealing their lollipops."

--Jeffrey Pelt (The Hunt for Red October)

Hypocrisy and politics go hand in hand. Nonetheless, ZH reminds us that although politicians tend to speak from both sides of their mouths, some of the then-vs-now quotes from this president are still capable of raising eyebrows.

"This administration acts like violating civil liberties is the way to enhance our security. It is not."

Well said. It channels the ideas of great statesmen like Benjamin Franklin and Patrick Henry. The problem is that this statement comes from Barack Obama--before he became president and in charge of the most powerful civil rights aggressor in existence.

Of course, it is not just politicians but also their minions that flip lids. As Nick Gillespie demonstrates, if their guy is in the White House, then people are more likely to be ok with Big Brother policies.

John Dahlberg, better known as Lord Acton, once said, "Power tends to corrupt, and absolutely power corrupts absolutely.

It appears that power particularly corrupts capacity for reason and for integrity.

--Jeffrey Pelt (The Hunt for Red October)

Hypocrisy and politics go hand in hand. Nonetheless, ZH reminds us that although politicians tend to speak from both sides of their mouths, some of the then-vs-now quotes from this president are still capable of raising eyebrows.

"This administration acts like violating civil liberties is the way to enhance our security. It is not."

Well said. It channels the ideas of great statesmen like Benjamin Franklin and Patrick Henry. The problem is that this statement comes from Barack Obama--before he became president and in charge of the most powerful civil rights aggressor in existence.

Of course, it is not just politicians but also their minions that flip lids. As Nick Gillespie demonstrates, if their guy is in the White House, then people are more likely to be ok with Big Brother policies.

John Dahlberg, better known as Lord Acton, once said, "Power tends to corrupt, and absolutely power corrupts absolutely.

It appears that power particularly corrupts capacity for reason and for integrity.

Saturday, June 15, 2013

FDR and the Gold Slackers

Hey you getting drunk, so sorry

I've got you sussed

Hey you smoking Mother Nature

This is a bust!

--The Who

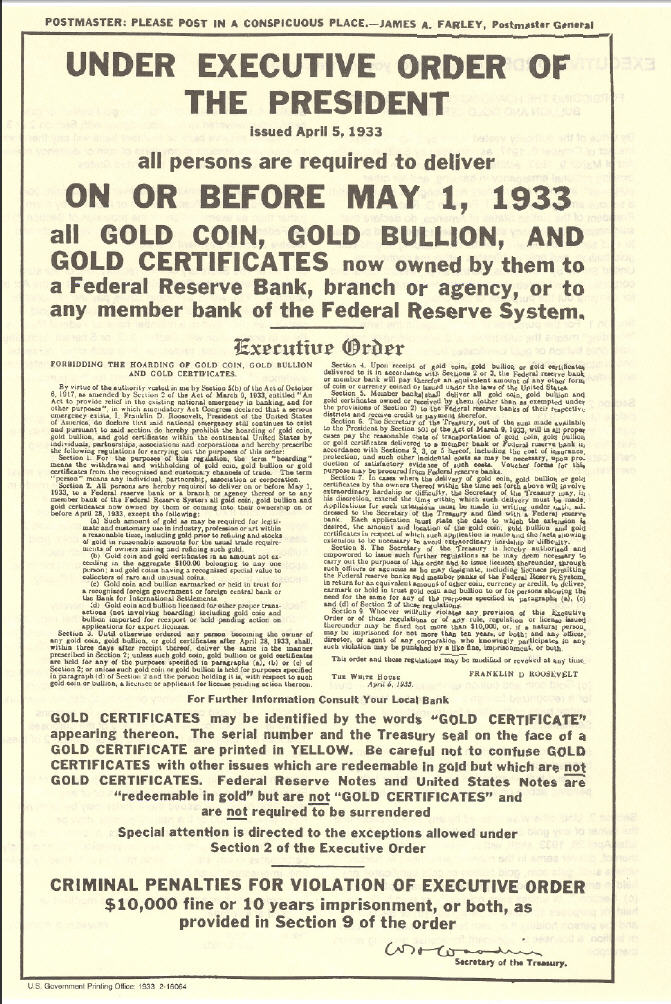

Eighty years ago this month FDR's gold confiscation order (Executive Order 6102) was being enforced.

And FDR's attorney general was publicly labeling people 'slackers' who did not turn in their gold.

The Roosevelt administration viewed this as warfare. The AG said:

"We are trying to win a war against depression and hard times...We are endeavoring to drive the gold out of hoarding. Each dollar that is held in hoard ties up from $15 to $20 in credit, or perhaps more. We are out to win this warfare."

Going into 1933, the dollar was still backed by gold. Citizens, and foreign trading partners for that matter, who felt uneasy about the federal government's monetary policy could go to the bank window and swap a $20 bill for roughly one ounce of gold. This is the discipline that a gold-back currency instills on policymakers. Either keep your inflationary urges in check, or people will drain gold from government vaults.

FDR employed aggression to overcome this problem. He confiscated the gold of US citizens. He further confiscated their property by devaluing the dollar. Because he broke the promise to repay creditors with gold if they chose, he also effectively defaulted on US government debt.

Some people suggest that the federal government couldn't do this again. After all, the dollar is no longer backed by gold, so what does the federal government care about where gold goes?

Perhaps, but gold can be viewed as a bet on disorder. Soaring gold prices signal that people are losing confidence in paper currency to the point where they will trade it for gold colored metal. Policy makers do not want to operate under such a signal.

The really interesting question isn't whether government might seek to confiscate gold again. It is whether people will obey next time around.

position in gold

I've got you sussed

Hey you smoking Mother Nature

This is a bust!

--The Who

Eighty years ago this month FDR's gold confiscation order (Executive Order 6102) was being enforced.

And FDR's attorney general was publicly labeling people 'slackers' who did not turn in their gold.

The Roosevelt administration viewed this as warfare. The AG said:

"We are trying to win a war against depression and hard times...We are endeavoring to drive the gold out of hoarding. Each dollar that is held in hoard ties up from $15 to $20 in credit, or perhaps more. We are out to win this warfare."

Going into 1933, the dollar was still backed by gold. Citizens, and foreign trading partners for that matter, who felt uneasy about the federal government's monetary policy could go to the bank window and swap a $20 bill for roughly one ounce of gold. This is the discipline that a gold-back currency instills on policymakers. Either keep your inflationary urges in check, or people will drain gold from government vaults.

FDR employed aggression to overcome this problem. He confiscated the gold of US citizens. He further confiscated their property by devaluing the dollar. Because he broke the promise to repay creditors with gold if they chose, he also effectively defaulted on US government debt.

Some people suggest that the federal government couldn't do this again. After all, the dollar is no longer backed by gold, so what does the federal government care about where gold goes?

Perhaps, but gold can be viewed as a bet on disorder. Soaring gold prices signal that people are losing confidence in paper currency to the point where they will trade it for gold colored metal. Policy makers do not want to operate under such a signal.

The really interesting question isn't whether government might seek to confiscate gold again. It is whether people will obey next time around.

position in gold

Friday, June 14, 2013

Why Hasn't Libertarianism Won the Day?

Benjamin Martin: May I sit with you?

Charlotte Selton: It's a free country. Or at least it will be.

--The Patriot

Nice reply by Tom Woods to some editorials written by people who oppose libertarianism. Libertarianism is the belief in societal design grounded in voluntary cooperation among individuals. Grounded in the philosophy of natural law, libertarianism posits that people are born with the right to pursue their interests as long as they don't forcefully interfere in the pursuits of others.

Libertarians oppose forceful aggression (a.k.a. the non-aggression principle). The only legitimate use of force is for self-defense. Viewed through the libertarian lens, the proper role of government is to help people defend their property (broadly construed to include life and liberty as well as material possessions) against aggression.

A question posed by one of the editorialists was this: If libertarianism is such a great framework, then why hasn't a country adopted it?

Before getting to Tom's response, I must first note that highly libertarian designs have been adopted at one time or another throughout history. Ancient Greece and Rome, for example, had runs that reflected may libertarian principles. Though not perfect, the system of government instituted by the United States, first under the Articles of Confederation and then under the Constitution, has been the boldest libertarian design in scale and scope enacted in the history of man.

The more accurate and interesting question to pose is this: Why has it been difficult for libertarian designs to persist?

Tom's response, which he frames as a series of rephrased questions, is based in large part on the axiom that people prefer leisure over work, and less work over more work. Stated differently, people want to get the most gain from the least amount of effort.

If people can advance their interests on the backs of others, then they are prone to do so. Because government is legalized force, then it is in the interest of some to use the strong arm of government to advance their interests at others' expense.

The history of the world can be seen as a battle of voluntary cooperation vs involuntary servitude. Peace vs aggression. Freedom vs force.

The libertarian design has been battling designs that employ aggression. Thus far, aggressive designs have had the upper hand. This obviously does not render the libertarian approach meaningless. It merely reflects the strength of human desire to force one's will onto others for personal gain.

Charlotte Selton: It's a free country. Or at least it will be.

--The Patriot

Nice reply by Tom Woods to some editorials written by people who oppose libertarianism. Libertarianism is the belief in societal design grounded in voluntary cooperation among individuals. Grounded in the philosophy of natural law, libertarianism posits that people are born with the right to pursue their interests as long as they don't forcefully interfere in the pursuits of others.

Libertarians oppose forceful aggression (a.k.a. the non-aggression principle). The only legitimate use of force is for self-defense. Viewed through the libertarian lens, the proper role of government is to help people defend their property (broadly construed to include life and liberty as well as material possessions) against aggression.

A question posed by one of the editorialists was this: If libertarianism is such a great framework, then why hasn't a country adopted it?

Before getting to Tom's response, I must first note that highly libertarian designs have been adopted at one time or another throughout history. Ancient Greece and Rome, for example, had runs that reflected may libertarian principles. Though not perfect, the system of government instituted by the United States, first under the Articles of Confederation and then under the Constitution, has been the boldest libertarian design in scale and scope enacted in the history of man.

The more accurate and interesting question to pose is this: Why has it been difficult for libertarian designs to persist?

Tom's response, which he frames as a series of rephrased questions, is based in large part on the axiom that people prefer leisure over work, and less work over more work. Stated differently, people want to get the most gain from the least amount of effort.

If people can advance their interests on the backs of others, then they are prone to do so. Because government is legalized force, then it is in the interest of some to use the strong arm of government to advance their interests at others' expense.

The history of the world can be seen as a battle of voluntary cooperation vs involuntary servitude. Peace vs aggression. Freedom vs force.

The libertarian design has been battling designs that employ aggression. Thus far, aggressive designs have had the upper hand. This obviously does not render the libertarian approach meaningless. It merely reflects the strength of human desire to force one's will onto others for personal gain.

Thursday, June 13, 2013

LIFO Bubbles and Japan

"You watch your tail, cowboy."

--Nick Conklin (Black Rain)

Peter Atwater thinks attention should focus on the sell-off in Japan and the associated spillover effects. Atwater suggests that the parabolic move in Japanese markets earlier this year reflected investor confidence in central bank ability to boost asset markets higher thru money printing. Once the last investor capable of becoming confident in central bank prowess does so, then the top in sentiment is in and the only place for confidence (and prices) to go is down.

He suspects that the harsh reversal in Japanese markets, both stocks and bonds, is a symbol that the top in central bank confidence has been put in. Because bubbles, he brilliantly observes, have a LIFO (last in first out) quality to them, the most extreme cases occur near the apex of confidence and are the first to turn. Because Japan has the makings of such an extreme case, market reversals there may signal that a systemic turn is now underway.

The Nikkei, btw, lost over 6% last night.

position in SPX, Treasuries

--Nick Conklin (Black Rain)

Peter Atwater thinks attention should focus on the sell-off in Japan and the associated spillover effects. Atwater suggests that the parabolic move in Japanese markets earlier this year reflected investor confidence in central bank ability to boost asset markets higher thru money printing. Once the last investor capable of becoming confident in central bank prowess does so, then the top in sentiment is in and the only place for confidence (and prices) to go is down.

He suspects that the harsh reversal in Japanese markets, both stocks and bonds, is a symbol that the top in central bank confidence has been put in. Because bubbles, he brilliantly observes, have a LIFO (last in first out) quality to them, the most extreme cases occur near the apex of confidence and are the first to turn. Because Japan has the makings of such an extreme case, market reversals there may signal that a systemic turn is now underway.

The Nikkei, btw, lost over 6% last night.

position in SPX, Treasuries

Why Should We Be Surprised?

"The government's been in bed with the entire telecommunications industry since the forties. They've infected everything. They get into your bank statements, computer files, email, listen to your phone calls...every wire, every airwave. The more technology used, the easier it is for them to keep tabs on you. It's a brave new world out there. At least it better be."

--Brill (Enemy of the State)

Ron Paul wonders why we should be surprised about the NSA surveillance scandal. Those who opposed the Constitution as written were among those who understood government's insatiable appetite for power and control.

Rights usually aren't forcefully taken overnight. Their erosion is gradual, steady. For instance, Judge Nap explains the erosion leading up to the present NSA situation.

We now face a situation similar to the colonists in the 1760s, who dealt with British soldiers writing their own search warrants to enter people's houses. That situation helped motivate a revolution and then a written Constitution meant to secure individual rights.

That Constitution has now been close to completely shredded.

With rights violated and Constitution shredded, what is likely to follow?

--Brill (Enemy of the State)

Ron Paul wonders why we should be surprised about the NSA surveillance scandal. Those who opposed the Constitution as written were among those who understood government's insatiable appetite for power and control.

Rights usually aren't forcefully taken overnight. Their erosion is gradual, steady. For instance, Judge Nap explains the erosion leading up to the present NSA situation.

We now face a situation similar to the colonists in the 1760s, who dealt with British soldiers writing their own search warrants to enter people's houses. That situation helped motivate a revolution and then a written Constitution meant to secure individual rights.

That Constitution has now been close to completely shredded.

With rights violated and Constitution shredded, what is likely to follow?

Wednesday, June 12, 2013

Laughing at Truth

I get all my papers and smile at the skies

Though I know that the hypnotized never lie

--The Who

Some fave media responses to the NSA incident and its implications over the past few days:

Though I know that the hypnotized never lie

--The Who

Some fave media responses to the NSA incident and its implications over the past few days:

Surveillance and Isomorphism

I try so hard not to get upset

Because I know all the trouble I'll get

--Til Tuesday

Jacob Hornberger observes that a primary objective of government surveillance is to keep people in line. The government collects information on people. If individuals rebel in some way, then government uses that information against them. For those who have not rebelled, the surveillance process serves as a signal to others about the benefits of compliance and the consequences of rebellion.

Surveillance is a process of institutional isomorphism. Its aim is compliance.

Because I know all the trouble I'll get

--Til Tuesday

Jacob Hornberger observes that a primary objective of government surveillance is to keep people in line. The government collects information on people. If individuals rebel in some way, then government uses that information against them. For those who have not rebelled, the surveillance process serves as a signal to others about the benefits of compliance and the consequences of rebellion.

Surveillance is a process of institutional isomorphism. Its aim is compliance.

Tuesday, June 11, 2013

Snowden's Remarkable Example

"It means if something's wrong, those who have the ability to take action have the responsibility to take action."

--Benjamin Franklin Gates (National Treasure)

Edward Snowden is the person who blew the whistle on the NSA record collection scandal. He is a rare person in today's world. An employee at government contractor Booz Allen, Snowden decided that he could no longer be a part of a process of massive surveillance of US citizens. He sacrificed a $200K/yr job, a dreamy Hawaiian lifestyle, and much of his liberty to tell the story.

He notes,

"If living unfreely but comfortably is something you're willing to accept--and I think many of us are, it's human nature--you can get up every day, you can go to work, you can collect your large paycheck for relatively little work, against the public interest, and go to sleep at night after watching your shows."

Snowden decided that he didn't want to do that anymore. And telling the truth set him free.

Will we learn from his example?

--Benjamin Franklin Gates (National Treasure)

Edward Snowden is the person who blew the whistle on the NSA record collection scandal. He is a rare person in today's world. An employee at government contractor Booz Allen, Snowden decided that he could no longer be a part of a process of massive surveillance of US citizens. He sacrificed a $200K/yr job, a dreamy Hawaiian lifestyle, and much of his liberty to tell the story.

He notes,

"If living unfreely but comfortably is something you're willing to accept--and I think many of us are, it's human nature--you can get up every day, you can go to work, you can collect your large paycheck for relatively little work, against the public interest, and go to sleep at night after watching your shows."

Snowden decided that he didn't want to do that anymore. And telling the truth set him free.

Will we learn from his example?

Monday, June 10, 2013

Institutional Isomorphism

"These walls are funny. First you hate 'em, then you get used to 'em. Enough time passes, you get so you depend on them. That's institutionalized."

--Ellis Boyd "Red" Redding

Institutional environments exude pressure for isomorphism, or sameness, among indiividuals who by definition are born different and unique. Processes that encourage institutional isomorphism can be mimetic, normative, or coercive in nature (DiMaggio & Powell, 1983; Meyer & Rowan, 1977; Scott, 1995).

Mimetic isomorphism occurs when individiuals, facing uncertainty, adopt the behavior of those perceived as successfully navigating the institutional environment. Who's staying alive? Who's getting promoted? What are they doing? Copy what appears to be working.

Normative isomorphism occurs when individuals adopt behavior patterns deemed to be appropriate in the institutional environment. Here's how we do things around here. Follow the rules. Keep your nose clean.

Coercive isomorphism occurs when institutional norms are imposed on individuals by force. If you do not comply, we will break you.

Individuals who bow to these pressures often want to be seen as belonging, i.e., as legitimate in the institutional field.

The larger and more powerful the institution, the greater the pressure for isomorphism.

References

DiMaggio, P. & Powell, W. 1983. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48: 147-160.

Meyer, A. & Rowan, B. 1977. Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83: 340-363.

Scott, R. 1995. Institutions and organizations. Thousand Oaks, CA: Sage.

--Ellis Boyd "Red" Redding

Institutional environments exude pressure for isomorphism, or sameness, among indiividuals who by definition are born different and unique. Processes that encourage institutional isomorphism can be mimetic, normative, or coercive in nature (DiMaggio & Powell, 1983; Meyer & Rowan, 1977; Scott, 1995).

Mimetic isomorphism occurs when individiuals, facing uncertainty, adopt the behavior of those perceived as successfully navigating the institutional environment. Who's staying alive? Who's getting promoted? What are they doing? Copy what appears to be working.

Normative isomorphism occurs when individuals adopt behavior patterns deemed to be appropriate in the institutional environment. Here's how we do things around here. Follow the rules. Keep your nose clean.

Coercive isomorphism occurs when institutional norms are imposed on individuals by force. If you do not comply, we will break you.

Individuals who bow to these pressures often want to be seen as belonging, i.e., as legitimate in the institutional field.

The larger and more powerful the institution, the greater the pressure for isomorphism.

References

DiMaggio, P. & Powell, W. 1983. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48: 147-160.

Meyer, A. & Rowan, B. 1977. Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83: 340-363.

Scott, R. 1995. Institutions and organizations. Thousand Oaks, CA: Sage.

Sunday, June 9, 2013

Easy Money Policy Favors the Rich

We are matching spark and flame

Caught in endless repetition

Life for life, we'll be the same

I must leave before you burn me

--The Fixx

This observation is consistent with something that we have noted frequently on these pages. Quantitative easing and other inventionary monetary policy favor the rich. The rich are the primary owners of stocks and other risky financial securities. Any policy geared toward boosting the prices of these risky assets, as QE purports to do, disproportionately benefits the wealthy.

Moreover, the decreased savings and increased borrowing promoted by easy credit policies are highly correlated to corporate profits. As interest rates are forced lower, people spend and borrow more, thus transferring economic resources to corporate balance sheets. Shareholders are the recipients of this wealth transfer.

Finally, interventions that ease monetary conditions always increase when asset prices decline. Owners of financial securities come to learn that their downside is limited because authorities will bail them out in the event of systemic decline. This moral hazard emboldens the rich to own even more stocks--because perceived risk has been artificially reduced by policy-makers.

As the article suggests, if you are rich, then why would you not conclude that, with government jacking prices higher and backstopping losses, the winning strategy is to acquire as many risky financial securities as you can?

position in SPX

Caught in endless repetition

Life for life, we'll be the same

I must leave before you burn me

--The Fixx

This observation is consistent with something that we have noted frequently on these pages. Quantitative easing and other inventionary monetary policy favor the rich. The rich are the primary owners of stocks and other risky financial securities. Any policy geared toward boosting the prices of these risky assets, as QE purports to do, disproportionately benefits the wealthy.

Moreover, the decreased savings and increased borrowing promoted by easy credit policies are highly correlated to corporate profits. As interest rates are forced lower, people spend and borrow more, thus transferring economic resources to corporate balance sheets. Shareholders are the recipients of this wealth transfer.

Finally, interventions that ease monetary conditions always increase when asset prices decline. Owners of financial securities come to learn that their downside is limited because authorities will bail them out in the event of systemic decline. This moral hazard emboldens the rich to own even more stocks--because perceived risk has been artificially reduced by policy-makers.

As the article suggests, if you are rich, then why would you not conclude that, with government jacking prices higher and backstopping losses, the winning strategy is to acquire as many risky financial securities as you can?

position in SPX

Saturday, June 8, 2013

Treasury Yields Not Giving Ground

Hey baby

There ain't no easy way out

Yeah I'll stand my ground

And I won't back down

--Tom Petty

Stocks rallied on Friday but bonds sold off. Ten year yields were +4% on the day and closed at the high for the recent move.

Thus far, long bond rates have not given back ground and remain above recently defined support at .205ish. Moreover, the TNX chart pattern is developing a bullish cup-and-handlish look.

Am tempted to add to my Treasury short which is about the only thing in my book currently 'working.'

How long will risk markets stomach days like this before carry traders start nervously eyeing the exits.

position in SPX and Treasuries

There ain't no easy way out

Yeah I'll stand my ground

And I won't back down

--Tom Petty

Stocks rallied on Friday but bonds sold off. Ten year yields were +4% on the day and closed at the high for the recent move.

Thus far, long bond rates have not given back ground and remain above recently defined support at .205ish. Moreover, the TNX chart pattern is developing a bullish cup-and-handlish look.

Am tempted to add to my Treasury short which is about the only thing in my book currently 'working.'

How long will risk markets stomach days like this before carry traders start nervously eyeing the exits.

position in SPX and Treasuries

Friday, June 7, 2013

Sweeping NSA Surveillance

"Careful, chief. Dig up the past, all you get is dirty."

--Lycon (Minority Report)

What would a week be without a new scandal surfacing about this administration? The scandal du jour is two massive NSA surveillance projects. One involves forcing Verizon (VZ), and likely other phone carriers, to hand over phone records of all its customers. The other involves a program that scours major Internet companies like Google (GOOG) and Facebook (FB) for data.

Once again, US mainstream media did not break this story. Instead, a reporter for the UK Guardian took the lead. This now makes at least five page one headline stories that Big Media in the US has whiffed on.

Yet, what could be a bigger story than a government that is hellbent on shredding the Constitution by violating people's rights on such a massive scale? This is the stuff of dictatorships, not republics.

As Judge Nap observes, the president, attorney general, and the judge who signed an open ended warrant are so blind to liberty that they are unworthy of their offices.

Many supporters of this administration are suggesting that Obama somehow does not own this problem because the Patriot Act was enacted under the Bush Administration. It's the juvenile 'He started it" argument that kids use to justify bad behavior on the playground.

We have said it before. If you inherit bad policy, you do not perpetuate or escalate it. You remove it.

no positions

--Lycon (Minority Report)

What would a week be without a new scandal surfacing about this administration? The scandal du jour is two massive NSA surveillance projects. One involves forcing Verizon (VZ), and likely other phone carriers, to hand over phone records of all its customers. The other involves a program that scours major Internet companies like Google (GOOG) and Facebook (FB) for data.

Once again, US mainstream media did not break this story. Instead, a reporter for the UK Guardian took the lead. This now makes at least five page one headline stories that Big Media in the US has whiffed on.

Yet, what could be a bigger story than a government that is hellbent on shredding the Constitution by violating people's rights on such a massive scale? This is the stuff of dictatorships, not republics.

As Judge Nap observes, the president, attorney general, and the judge who signed an open ended warrant are so blind to liberty that they are unworthy of their offices.

Many supporters of this administration are suggesting that Obama somehow does not own this problem because the Patriot Act was enacted under the Bush Administration. It's the juvenile 'He started it" argument that kids use to justify bad behavior on the playground.

We have said it before. If you inherit bad policy, you do not perpetuate or escalate it. You remove it.

no positions

Thursday, June 6, 2013

Everyone Will Lose

"You hear that Mr Anderson? That is the sound of inevitability."

--Agent Smith (The Matrix)

As interventionist policy has escalated, many investors have been searching for ways to hedge against the inevitable--against the time when intervention can no longer restrain market forces seeking to move the system back into natural balance.

While some hedges are certainly available, there is no perfect hedge. In the case of monetary collapse, for example, even someone who owns a boatload of gold will be stung by spiraling prices.

Everyone will lose to some degree.

An investor can only hope to do his/her best to minimize the damage that is coming. To emerge on the other side as whole as possible--knowing full well that the outcome will be a fraction of before.

position in gold

--Agent Smith (The Matrix)

As interventionist policy has escalated, many investors have been searching for ways to hedge against the inevitable--against the time when intervention can no longer restrain market forces seeking to move the system back into natural balance.