"The new law of evolution in corporate America seems to be survival of the unfittest. Well, in my book you either do it right, or you get eliminated."

--Gordon Gekko (Wall Street)

'Private equity' has been thrust into the forefront because Republican presidential hopeful Mitt Romney used to head

Bain Capital, a large private equity firm. Private equity firms amass capital (which may be equity or debt financed) and take ownership stakes in businesses. Usually, although not always, these ownership stakes result in the companies going private if they were not already so.

While they sometimes invest in nascent industries and enterprises, private equity firms are more prone to scour mature industries for under-performing companies with commensurately low valuations. By purchasing controlling ownership stakes, private equity firms then act to make operations more productive. If the productivity improvements are successful, then profits are likely to rise. With rising profits come rising valuations. The benefits of higher valuation may then be realized by selling part or all of the company to another private owner, taking the company public (IPO), or operating the company as an ongoing concern.

Of course, it is also possible that the investment does not work out, in which case the private equity firm may either sell the company at a loss, file for bankruptcy, or operate the company as an ongoing concern.

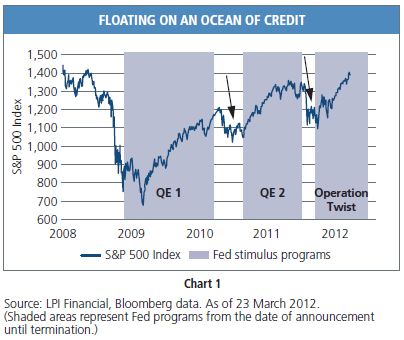

From an investment perspective, private equity is considered an 'alternative asset class.' Alternative investments are asset classes with potential to produce returns that are uncorrelated to conventional stock and bond returns. Other alternative asset classes include commodities, venture capital, and hedge funds. As investors have become more sophisticated, alternative assets have become a popular way to diversify portfolios, particularly among institutional investors (e.g., pension funds, endowments). Portfolio managers have thus poured oceans of capital into private equity funds. Private equity funds under management are estimated at $2+ trillion dollars.

Thus, many Americans, particularly those with defined benefit plans, have ownership stakes in private equity.

There is good reason for this. The social value of private equity operations is that they improve efficiency of scarce economic resources. Unproductive operations squander economic resources, which drags down general standard of living. Reconfiguring under-performing operations toward more productive ends creates more output per unit of input. Inputs such as labor or materials that are no longer needed in the streamlined operations can subsequently seek more productive uses. Society is better off.

This missive includes a partial review of research confirming the benefits of private equity operations.

Unfortunately, what captures the attention of many are the layoffs that often occur during productivity improvement efforts. Predictably, the Obama administration

has jumped on this bandwagon, painting candidate Romney as a heartless soul who shuts down factories in pursuit of profits. With

notable exceptions, the media happily play along.

Hazlitt

has eloquently explained the error (a chronic one at that) of this line of thought.

To be sure, there are problems with the private equity model as currently practiced. Artificially cheap credit offered by central banks provides a level of funding for private equity projects unavailable if borrowing were based market-determined interest rates. Moreover, suppressed yields on more conservative investment vehicles has more portfolio managers seeking riskier positions, thereby showering private equity projects with far more funds than they otherwise would. Finally, the gigantic degree of leverage in the credit-induced financial system shrinks investment time horizon, making private equity operators and their investors more sensitive to short term outcomes than they would be in a less leveraged world.

In short, government intervention has surely inflated private equity projects far beyond their 'natural' reach. It has also made private equity investors less patient--i.e., more prone to prematurely pull the plug on projects might produce better results if given more time.

Of course, few government officials or mainstream media outlets are likely to take on this facet of private equity...

I do wonder whether the president may be unwittingly

digging a hole for himself by attacking the idea of private equity operations. If Romney counters correctly, then the debate could morph into the merits of unhampered markets seeking the best use of scarce resources vs socialized markets that shelter and encourage under-performance.

American most desperately needs a full-throated debate on this issue. Perhaps private equity has 'funded' such a debate.

![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_s3o8xjyXW5DGdk4fH-KBVCh7i7XT5LMb0Riwy3uk3HxSinUEqamzM-rfiDAfNyyLPt5gKJxk7i0xPuXn90Vg7eAG292xepT4mF5worH4yHsOYOyh82J56OFbsTbcOaAgQDog=s0-d)